ecoPayz Casino Withdrawals: Payout Speeds and Cash-Out Limits

Processing Delays: What Happens During Casino KYC Checks

The conversation I have with players about withdrawals has barely changed in eight years. It goes like this: “I deposited in seconds, why does cashout take a day?” The deposit-versus-withdrawal asymmetry is the single most frustrating thing about online casino play, and it’s also the most misunderstood.

What's inside this guide

The honest answer is that a deposit is a one-stage event — the casino accepts your money and updates the balance — while a withdrawal is a four-stage event with each stage owned by a different party. The casino reviews. The casino approves. Payz credits. And, optionally, the Mastercard route adds a fourth stage. Each stage has its own clock, its own checks, and its own ways of breaking.

This piece is a stage-by-stage walkthrough of where the time goes, what triggers a hold, where the tier-based limits bite, and what to do when something genuinely sticks. No “instant” promises — I don’t make them, because they aren’t realistic in the post-2025 enforcement environment.

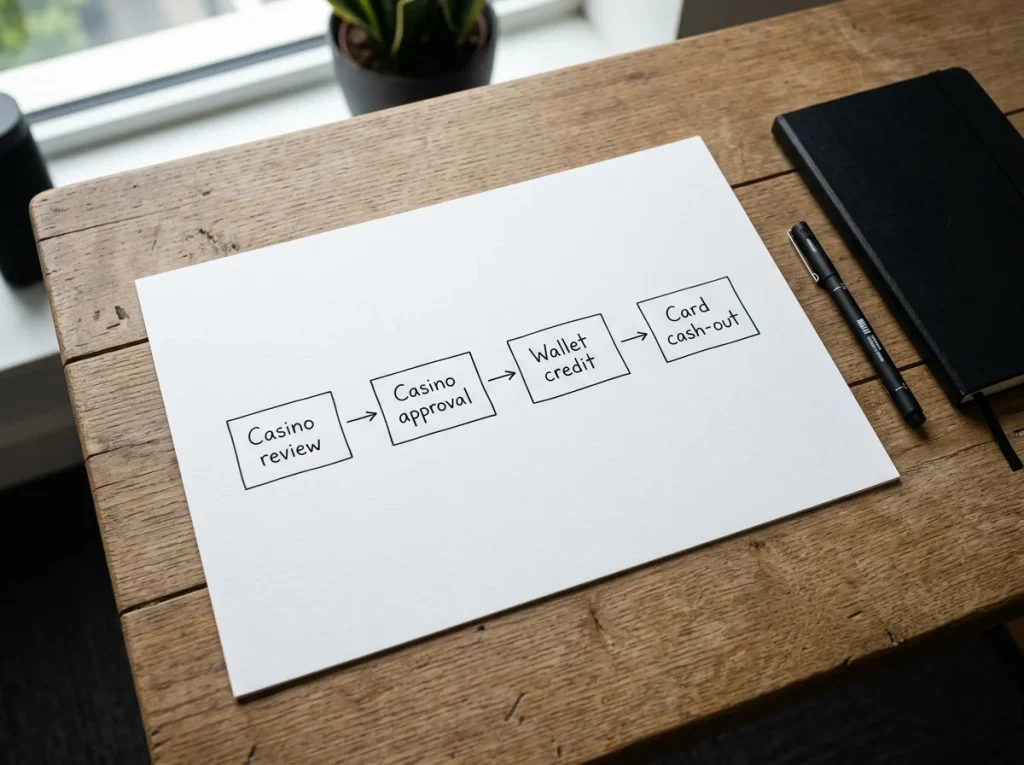

The four stages of a withdrawal, mapped end to end

The single most useful mental model for understanding withdrawal timing is to break the payout into four sequential stages, each with a different actor and a different set of rules.

Stage one is casino-side review. When you submit a withdrawal request, the casino’s risk and compliance system inspects the account, the play pattern, the source of the funds, and the destination. For a verified player with no flagged activity, this stage runs in minutes to hours. For an account with unresolved KYC items, a play pattern that triggers AML scoring, or a withdrawal-method change from the deposit method, it can stretch to days.

Stage two is casino-side approval. Once review clears, the operator’s payments team — sometimes automated, sometimes manual — pushes the payout into the outbound queue. Most large operators run this queue continuously during business hours and at lower frequency overnight and at weekends. A withdrawal approved at 2 PM on a Tuesday hits the wallet sooner than the same withdrawal approved at 11 PM on a Sunday.

Stage three is Payz-side crediting. Once the casino has released the funds, Payz’s settlement infrastructure receives them and credits your wallet balance. PSI-Pay’s framework supports €3 billion in global transactions through its underlying infrastructure, which is plenty of headroom for normal-volume crediting; the Payz leg is typically the fastest of the four stages, measured in seconds to minutes once the casino has actually released.

Stage four is optional. If you want spendable cash rather than a wallet balance, you’ll load the funds onto your Payz Mastercard and withdraw or spend from there. This stage has its own clock — usually fast for the wallet-to-card transfer, but constrained by the daily caps on the card itself — and it only fires if you choose the card route.

The pattern across hundreds of withdrawal logs I’ve reviewed: stages one and two account for almost all the elapsed time. Stage three is fast. Stage four is fast but constrained by daily caps. So when a player tells me their withdrawal “is slow”, what they’re describing is a stage-one or stage-two delay, and the right diagnostic is to look at the casino’s status messages rather than blaming the wallet.

How long the casino actually takes and why

The casino-side stages have stretched in 2025 and into 2026, and there’s a clear regulatory reason. Two enforcement actions in November 2025 are worth understanding, because they shaped how UKGC operators now approach withdrawals across the board.

Videoslots Limited paid a £650,000 fine on 20 November 2025 for AML and social responsibility failures, including findings that the operator’s monthly deposit limits had been ineffective in practice and that controls around certain payment-method routes — specifically pre-paid digital vouchers used for gambling — had operated without effective oversight. Two weeks earlier, on 5 November 2025, NetBet Enterprises Limited received an identical £650,000 fine plus a mandatory independent audit for AML and SR failures with overlapping characteristics.

The combined effect of those two enforcement actions, plus the broader pattern of 13 regulatory cases between May and December 2025, is that UKGC operators have tightened their withdrawal-review processes materially. Withdrawals that would have cleared review in an hour in 2023 now routinely take three to six hours, with longer holds applied to accounts where the play pattern or the deposit-method history shows anything the AML system finds worth checking.

What casinos look at during this review is consistent across the industry: source of deposit funds (e-wallet vs card vs bank), the deposit-to-withdrawal ratio in the current account period, any recent change to verification details, any unresolved bonus terms, and whether the withdrawal route matches the deposit route. A Payz-funded account requesting a Payz withdrawal of less than the cumulative deposit balance, with stable verification details, is the cleanest case and clears review fastest.

The withdrawal route matching the deposit route is a regulatory expectation, not just an operator preference. It exists to prevent money-laundering patterns where deposits flow through one channel and withdrawals exit through a different one. If you’ve funded through Payz, your first withdrawal of up to the cumulative deposit amount should go back to Payz. Trying to redirect to a bank account or a card on file will usually trigger an additional verification step that adds hours.

What Payz itself adds to the clock

Once the casino has released funds, the Payz-side stage is short by comparison, but it has its own moving parts worth understanding.

The infrastructure handling this leg sits inside PSI-Pay’s framework, which supports €3 billion in global transactions across the Payz product family. That capacity headroom matters because it means even a busy weekend with high payout volume across UK operators doesn’t queue at the Payz layer — the receiving capacity is there. PSI-Pay’s 2024 accounts show total assets of £64.97 million and the firm’s standing as a Principal Member of Mastercard since 2009, which together describe an institution with the liquidity and the regulatory framework to settle inbound payouts without delay.

The Payz-side stage is split into two parts. The first is the actual credit to your wallet balance from the casino’s outbound payment. That’s usually instantaneous to a few minutes — the casino sends, Payz receives, the balance updates. The second is any internal velocity or anti-fraud check the Payz system runs on the incoming credit, which can hold a credit for additional review in edge cases. The most common trigger is an unusually large inbound credit relative to the account’s normal activity, or an inbound credit following a recent KYC tier change.

For a typical UK player whose account sits at Classic or Silver, with regular deposit-and-withdrawal activity at consistent amounts, the Payz-side stage runs in single-digit minutes. For players whose accounts haven’t seen a withdrawal in months and suddenly receive a large one, expect Payz to add a check to confirm the credit is legitimate. This isn’t an obstruction; it’s exactly the safeguarding posture that the FCA’s e-money regime expects.

If the Payz-side stage is slow, the wallet app’s transaction log will show the incoming credit with a “pending” status. That status is informative — it tells you the funds have arrived but not yet been released for use. Once the internal check clears, the status flips to “completed” and the balance becomes available.

How your Payz tier maps to withdrawal caps and KYC

The tier you sit on inside Payz determines two things that matter for withdrawals: the per-transaction and rolling-period caps on outgoing transfers, and the depth of KYC required to operate at that tier.

Classic, the entry tier, has the lowest caps but the lightest KYC. After basic identity verification — passport or driving licence, address proof — you can withdraw up to a defined daily and monthly headroom that suits most UK casual play. The Classic-tier FX rate of 2.99 per cent applies on cross-currency withdrawals; same-currency withdrawals don’t trigger it.

Silver expands the limits with additional KYC. You upload further documentation, the wallet runs additional checks, and your headroom on outbound transfers grows. The FX rate at Silver stays the same as Classic.

Gold drops the FX rate to 1.49 per cent and expands the limits further, but requires source-of-funds documentation in addition to identity verification. This is a meaningful step up: the source-of-funds package typically includes recent bank statements, payslips or employer documentation, and sometimes a written explanation of the funding source for larger balances. The point of the additional KYC is not bureaucracy for its own sake — it’s the standard EMR regime expectation that an authorised e-money institution like PSI-Pay knows where high-volume client funds are coming from.

Platinum drops the rate to 1.25 per cent and further expands the limits, with corresponding KYC depth. True VIP runs on bespoke terms outside the public ladder.

For a casino player thinking about withdrawals, the practical question is whether your withdrawal pattern actually pushes the Classic limits. For most UK players cashing out a few hundred pounds at a time, Classic is sufficient. For a player who’s had a substantial win and wants to move four or five figures out in one or two transactions, the Silver or Gold tier headroom may matter, and the KYC step needs to happen before the withdrawal, not during it.

One detail that catches players out: upgrading mid-withdrawal doesn’t accelerate the current request. The casino has already locked in the route and the tier at the moment you submitted the request. The upgrade applies to subsequent withdrawals, not to the one already in flight.

What the Mastercard cashout route actually looks like

The Payz Mastercard route is the fastest path to spendable cash, with constraints worth understanding before you choose it over a bank-transfer cashout.

The route is straightforward: once your withdrawal has landed in your Payz wallet balance, you transfer it onto your Payz Mastercard. The wallet-to-card transfer is usually instantaneous, and the card is then usable for purchases or ATM withdrawals. Because PSI-Pay holds Principal Member status with Mastercard and issues its own cards across 173 countries and 44 currencies, the card sits inside the standard Mastercard scheme — accepted wherever Mastercard is, with the same chargeback rights and the same dispute mechanisms as any other Mastercard product.

The caps are where the constraint shows up. The maximum single contactless transaction in the UK is £100 or equivalent, which means you can’t tap a £300 purchase in one go — it would need to be split, or done via chip-and-PIN rather than contactless. The daily ATM cash withdrawal limit runs up to €750 equivalent, and the daily purchase ceiling sits at €5,500 equivalent. Those daily caps reset at midnight in the card’s home time zone, not at midnight your time.

For a £2,000 withdrawal that you want fully in cash via ATM, the daily cap of €750 (about £650 depending on the day’s rate) means three or four separate visits across three or four days. Each ATM visit carries the ATM operator’s own withdrawal fee, which Payz doesn’t control. Cumulatively, that’s a noticeable cost compared to a single bank-transfer cashout.

For a £200 withdrawal that you want spendable for purchases — say, paid out into the card and used for groceries and other purchases over the week — the card route is essentially free in fee terms (the wallet-to-card transfer carries no meaningful charge at most tiers) and as fast as instant.

The decision between Mastercard route and bank-transfer route is therefore a question of urgency and amount. Large amounts go via bank to save the ATM fees and the daily caps. Small amounts go via card for speed.

What the wallet actually charges to send money out

Withdrawal fees on the Payz side are tier-dependent and route-dependent, and the structure rewards either climbing the ladder or batching your cashouts rather than spreading them across many small transactions.

The bank-transfer route — from Payz wallet to your UK bank account — carries a per-transaction fee that scales down at higher tiers. At Classic the fee is the highest in the ladder; at Platinum it’s materially lower. The fee is sterling-denominated and flat, so it bites harder on small withdrawals than on large ones. A £50 withdrawal that pays a fee of a few pounds is paying a noticeable percentage; a £500 withdrawal paying the same flat fee is paying a fraction of a percent.

The Mastercard-load route — from Payz wallet to your Payz Mastercard — carries a smaller transfer fee or none at all, depending on tier. The “fees” associated with the card route come at the point of use rather than the point of transfer: ATM-operator fees, FX margins if cross-currency, and the cap-related cost of having to split a large withdrawal across multiple days.

The wallet-to-wallet route — from one Payz user to another — is the cheapest in absolute terms but doesn’t usually feature in a casino-withdrawal workflow.

The FX consideration is separate. If your Payz balance is in EUR and the casino paid you in GBP, the conversion margin already applied at the moment the inbound credit landed. The withdrawal-side fee is on top of that, applied at the moment you push funds out of the wallet. Same-currency withdrawals from a same-currency balance never trigger the FX layer — Classic’s 2.99 per cent never fires, Gold’s 1.49 per cent never fires.

The weekly and monthly caps that catch players out

Beyond the per-transaction limits, there are rolling-period caps that catch players out specifically when they’ve had an unusually large win and want to move it out quickly.

The Payz wallet has weekly and monthly outbound caps that scale by tier. A Classic-tier account has the lowest rolling caps; a Platinum-tier account has the highest. These caps reset on a rolling seven-day or thirty-day window, not on a calendar week or month, which sometimes surprises players who expect a Sunday-to-Sunday reset.

The casino has its own withdrawal caps that operate alongside the wallet’s. UKGC-licensed casinos typically advertise a maximum daily withdrawal and a maximum weekly or monthly withdrawal that’s substantially higher than the daily figure. For a £20,000 single payout — a serious slot or live-dealer win — most casinos will pay out in tranches across days or weeks rather than in a single lump, regardless of which payment method is selected.

The interaction between casino caps and wallet caps is the binding-constraint problem: the lower of the two wins. If your casino allows £5,000 a day and your Payz Classic-tier daily cap is £2,000, the £2,000 wins. If your casino caps at £2,000 and your Payz allows £5,000, the £2,000 still wins. The order of operations matters: the casino releases funds first, so the casino’s cap is what determines how much can hit the wallet on any given day; the wallet’s cap then governs how much can leave the wallet on the same day.

For a large payout, the right move is usually a planned multi-day cashout: agree the schedule with the casino if necessary, request the daily maximum each day, and let the wallet caps stay below the binding casino constraint. Trying to push the maximum on both layers in one day usually results in one or the other rejecting the request, with the failed attempt potentially flagging the account for additional review.

When the request genuinely stalls and what to actually do

Sometimes a withdrawal genuinely sticks — not the normal four-to-six hour review, but a hold of a day or more with no clear status update. The diagnostic process is straightforward if you know where to look.

First, check the casino-side status. The cashier or the account history should show the withdrawal as “pending review”, “pending approval”, “processing” or similar. If it’s been in “pending review” for over 24 hours, that’s unusual for a verified account and worth flagging to the casino’s support. If it’s “processing”, the casino has approved and the funds should be in the Payz inbound queue.

Second, check the Payz-side status. Open the Payz app and look at the recent transactions. An inbound credit from the casino should appear as a pending or completed line item. If there’s no inbound credit visible, the casino hasn’t released yet — escalate on the casino side, not the wallet side.

Third, if the inbound credit is visible on the Payz side as “pending” for more than a few hours, contact Payz support directly. This is rare but does happen if the credit triggered an internal anti-fraud check that needs manual clearance.

Fourth, if both sides show the transaction as complete but the funds aren’t usable, the issue is almost certainly an account-side restriction. Some operators apply a holding period during which approved withdrawals can be reversed back into the casino balance — usually with a defined window, sometimes labelled “reverse withdrawal” or “pending review window”. UKGC guidance has tightened on this practice; John Pierce, UKGC Director of Enforcement, has been explicit in recent enforcement contexts that operators must apply their controls “to the standards we expect”, and that includes clear and prompt withdrawal handling. Persistent reversal-window holds beyond what the operator’s T&Cs advertise are worth escalating both to the operator and, if unresolved, to the operator’s licensed dispute-resolution service.

A deeper diagnostic walkthrough — including what specific status codes mean and how to interpret AML-related holds — is in the dedicated withdrawal-delays guide for players whose withdrawals have stuck longer than the patterns I describe here.

Why does the casino mark my Payz withdrawal as "pending" before sending it for review?

The "pending" state is the casino"s holding period before the withdrawal enters the actual review queue. It exists for two reasons: to give the player a chance to cancel and reverse the withdrawal back into the casino balance, and to batch withdrawal requests for the review team to process efficiently. The pending state typically lasts from a few hours to up to 24 hours depending on the operator. If the operator"s T&Cs specify a maximum pending window, that"s the figure to hold them to; anything materially longer than the advertised window is worth raising with support.

Does upgrading my Payz tier in the middle of a withdrawal speed up that specific cashout?

No. The withdrawal is locked to the tier you sat on at the moment you submitted it. A mid-withdrawal upgrade — completing additional KYC, moving from Classic to Silver or Gold — applies to subsequent withdrawals, not to the one already in flight. The current withdrawal will run on the original tier"s limits, FX rate and fee structure. If you anticipate needing the higher tier"s limits or FX rate, complete the upgrade before initiating the withdrawal, not during it.

If my Payz Mastercard has expired during the review, do my winnings still arrive on the Payz balance?

Yes. The withdrawal lands on your Payz wallet balance regardless of the Mastercard"s status. The Mastercard is a separate funding instrument loaded from the wallet; it isn"t on the path the casino sends funds along. If your card has expired, the funds will sit on the wallet balance until you order a replacement card, request a new physical or virtual card, or use the bank-transfer route to move the balance to your bank account instead.

Why does the casino sometimes ask for new ID documents during a withdrawal even though I"m already verified?

UKGC-licensed operators are required to apply ongoing customer due diligence, not just upfront KYC. A withdrawal at a threshold the operator"s risk policy treats as significant — common thresholds are around £2,000 cumulative — can trigger a refresh of identity documents, address proof, or source-of-funds evidence. This is regulatory expectation rather than operator pickiness. Providing the documents promptly is the fastest way to clear the hold; arguing with support that you were verified previously rarely accelerates anything.

ecoPayz Casino Articles: UK Market Trends and Payment Data

Written by the editors at Ecopayz Casino UK.