ecoPayz Casino Fees: Tier FX Rates and Withdrawal Costs

Real Transaction Costs vs Advertised Tier Rates

The single biggest mistake British players make with Payz fees is reading the deposit page, seeing “free”, and stopping there. I’ve sat with players who spent the better part of a year convinced their e-wallet was costing them nothing, only to discover that a quiet FX margin on every cross-currency deposit had eaten the equivalent of two months of casual play.

What's inside this guide

The real picture is layered. There’s the tier-locked FX rate that triggers whenever your wallet currency doesn’t match the casino currency — 2.99 per cent at Classic, 1.49 per cent at Gold, 1.25 per cent at Platinum and True VIP. There’s the withdrawal-side fee that lands when you push money back out of the wallet. There’s the casino-side fee that the operator may apply on top. And there’s the Mastercard cash-out cost if you choose the card route to get to spendable cash quickly.

This piece is the calculator-grade walkthrough I’d hand a friend who asked. Numbers, layers, worked examples — no marketing.

To avoid unexpected charges when upgrading your account, it is highly recommended to review the ecoPayz Classic tier limits before transferring large sums.

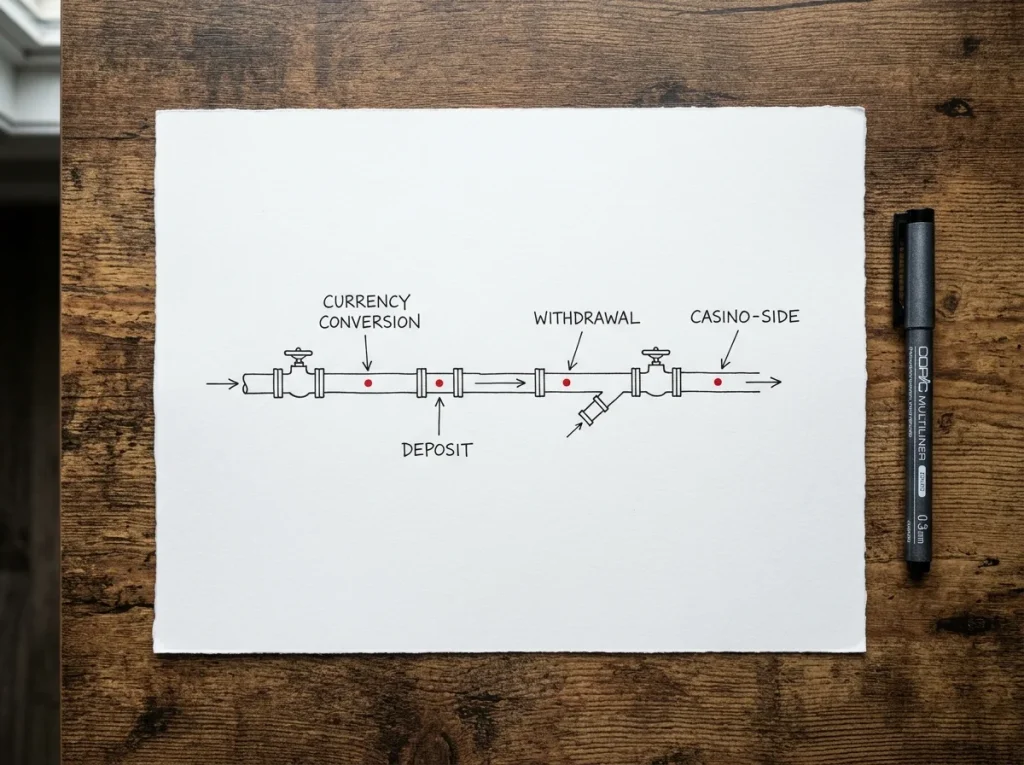

The four places a fee can actually land

If you map a single casino deposit and the eventual withdrawal end-to-end, there are four distinct moments where money can leak out of your balance. Most players see one of them, sometimes two. The fourth almost never makes it into a comparison article because it only fires under specific conditions.

The first leak point is currency conversion on the way in. If your Payz balance is in GBP and you deposit at a GBP casino, this layer is silent. The moment your wallet sits in EUR, USD or any other currency and the casino debits in GBP, Payz applies the tier-locked FX margin. At Classic that’s 2.99 per cent on the converted amount; the rate is fixed by your tier and doesn’t move within the day.

The second leak point is the deposit-side per-transaction charge. On Payz itself, casino deposits are usually free — the operator pays the merchant fee on the receiving side. There are exceptions for funding methods that load Payz itself (a Mastercard deposit into your wallet from an external source has its own cost), but the wallet-to-casino leg is clean.

The third leak point is the withdrawal back out of Payz, either to your bank account or onto the Payz Mastercard for cash access. The withdrawal-side fee structure varies by tier and by route, with Mastercard cash-out carrying the £100 contactless ceiling and the €750-equivalent daily ATM cap.

The fourth leak point — the one almost no one sees coming — is the casino-side fee that some operators apply to specific payment methods. UKGC-licensed casinos can’t charge a fee on deposits as such, but they can structure their cashout terms in ways that make e-wallet routes more or less expensive than card routes for the player. I’ll come back to this. Together those four layers determine the true all-in cost, and looking at any single one in isolation is how players get blindsided.

What each Payz tier actually charges on FX

The Payz tier ladder is the most important fee schedule in this article, because it’s the one that scales with how much you transact and how much paperwork you’ve already cleared. Four operational tiers matter for most UK players: Classic, Silver, Gold, Platinum. The True VIP tier exists above Platinum but works on bespoke economics and isn’t a tier you set yourself toward in the public-facing ladder.

Classic is the entry rung. After you verify your identity with the standard ID-plus-address-proof package, you sit at Classic and your cross-currency conversion charge is 2.99 per cent. Skrill and Neteller, the two e-wallets people most often compare Payz against, both charge 3.99 per cent at their equivalent entry tiers — so even on day one without climbing the ladder, Payz is materially cheaper for cross-currency activity.

Silver is a verification step rather than a fee step. You clear additional KYC checks, your transaction limits expand, but the headline FX rate stays at 2.99 per cent. Silver isn’t where the cost story changes; it’s where you unlock more headroom for larger deposits and withdrawals.

Gold is the first tier where the FX margin actually drops. At Gold the rate falls to 1.49 per cent — exactly half of the Classic charge — but the tier carries a monthly maintenance fee in fee-or-spend equivalent. For a player whose cross-currency volume is high enough, the FX saving more than covers the monthly cost. For a casual player who deposits monthly in a single currency, Gold’s monthly fee turns out to be expensive padding.

Platinum drops the rate to 1.25 per cent. The monthly maintenance scales up accordingly, and the volume thresholds to qualify rise. At True VIP, the headline rate stays at 1.25 per cent but the conditions are negotiated rather than scheduled.

The number to internalise is the ratio: Platinum’s 1.25 per cent is roughly 42 per cent of Classic’s 2.99 per cent. For a cross-currency player at meaningful volume, that’s not a marginal saving — it’s a structural shift in how much the wallet leg of every deposit costs. For a same-currency player, every one of those tier rates is zero in practice because FX never fires.

What the deposit costs you on the way in

The deposit-side fee picture on Payz is, by the standards of payments, blessedly clean. The wallet doesn’t charge you to push money out to a casino. The casino, in most UKGC-licensed cases, doesn’t charge you to receive money via Payz. So the deposit itself, on a same-currency leg, is genuinely free.

The complications start when you have to top up the Payz wallet itself before depositing. Payz accepts wallet funding via bank transfer, debit card and a few alternative routes, each with its own cost profile. Debit card top-ups are typically free or near-free; bank transfers usually take longer but cost less; certain reload routes carry small percentage charges. None of these is a casino fee — they’re wallet-funding fees — but they land in the same week as your deposit and feel like part of the same transaction.

There’s a second deposit-side cost players don’t think about: the time-cost of being mis-tiered. With 80 per cent of online gamblers funding play from a phone, the deposit flow is optimised for speed, and players default to whatever tier their wallet currently sits on. If you’ve been on Classic for two years and your cross-currency volume has crept up, you may have been paying 2.99 per cent on a hundred deposits when a tier upgrade would have dropped you to 1.49 per cent. The wallet doesn’t prompt you to upgrade — that’s on you.

The third quiet cost is rounding. When the casino’s cashier accepts a deposit in its display currency and converts on the wallet side, the FX margin is applied to the converted amount, not the deposit value you typed. A £100 deposit funded from a EUR balance becomes a EUR debit at the day’s mid-market rate plus the Classic margin. The casino sees £100; you see something slightly more in EUR than the mid-market rate would suggest. Over a hundred deposits that rounding-and-margin combination becomes a recognisable line item in your annual play cost.

None of these layers makes Payz expensive in absolute terms. They’re below the cost of using a debit card or a credit-card-substitute route. But they’re not zero, and treating them as zero is how the all-in cost gets understated.

What the withdrawal costs you on the way out

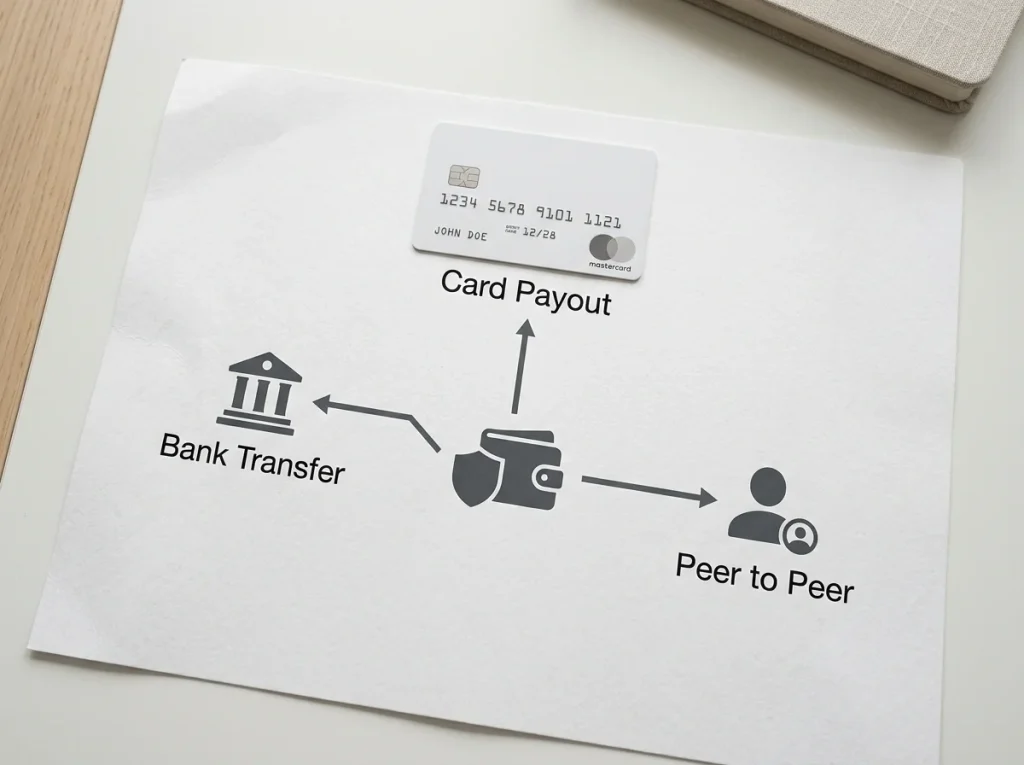

Withdrawal fees are where the e-wallet payments world gets messier than the deposit side, and where Payz’s tier ladder shows its edge most cleanly. There are three withdrawal routes from a Payz balance: back to bank account via transfer, onto the Payz Mastercard for cash and spending, or — less commonly — to another wallet via an internal transfer.

The withdrawal-to-bank route from a Payz balance carries a fixed sterling charge that scales down by tier. At Classic the per-withdrawal fee is the highest in the ladder; at Platinum it’s materially lower. For a player who cashes out once a month, the per-transaction fee on the bank route adds up modestly. For a player who cashes out weekly, it compounds noticeably and is one of the strongest arguments for climbing the tier ladder.

The withdrawal-to-Mastercard route involves card-scheme costs rather than a flat Payz fee. You load your Mastercard from your wallet balance, and then you use the card. The wallet-to-card transfer itself is usually fee-free or near-free; the cost comes when you actually use the card — at an ATM with its own withdrawal fee, or on a purchase that may carry an FX margin if it’s cross-currency.

The withdrawal-to-other-wallet route — sending from Payz to another Payz user — is the cheapest in absolute terms but rarely useful for a casino player. It exists mostly for peer-to-peer use cases.

The Payz liquidity picture is worth a sentence here, because withdrawal speed and fee structure both depend on it. PSI-Pay’s 2024 accounts show total assets of £64.97 million and net income of £260,634 — a small institution by consumer-fintech standards, but with the regulatory perimeter and Mastercard Principal Member backing to settle normal-volume withdrawals without delay. The bottleneck on UK casino payouts is almost never the wallet’s liquidity; it’s the casino-side review queue, which is a different fee-adjacent story I unpack in the worked examples below.

One detail almost no one accounts for: dormancy. If you withdraw to your wallet, hit a busy patch of life, and let the balance sit there for a year or more, dormancy fees may start eating the balance from the inside. Withdraw all the way out, not just out of the casino.

What the casino itself adds on top

The UK Gambling Commission’s licensing conditions effectively prohibit operators from charging direct deposit fees to consumers. So when you read a UKGC casino’s cashier and it shows “0% fee” next to Payz, that’s not marketing — it’s a regulatory floor.

But “deposit fees” and “all-in casino cost” are not the same thing. There are several legitimate operator-side mechanisms that affect what your money actually buys, none of which is a fee in the strict cashier sense.

The first is bonus eligibility. If a casino’s welcome offer or reload promotion excludes e-wallet deposits, the deposit went through fee-free but you also went through bonus-free. That’s not a fee, but it’s an opportunity cost the cashier doesn’t display. The exclusion language is usually buried in T&Cs; some operators publish it cleanly in the bonus terms, others tuck it into a payment-methods sub-page.

The second is wagering contribution. Even when an e-wallet deposit qualifies for a bonus, some operators count e-wallet-funded wagers at a reduced rate towards rollover. A £100 wagered on slots from a Payz deposit might count as £75 toward wagering requirements. Again, not a fee in cash terms, but a real economic effect.

The third is withdrawal-method tying. Some operators require the withdrawal route to match the deposit route — if you funded with Payz, you must cash out to Payz first, up to the deposit amount, before any other route opens. This isn’t a fee, but it can affect the all-in cost if your wallet currency forces an FX conversion that wouldn’t have happened on a bank route.

The fourth is currency. Casinos that display in EUR or USD apply their own internal rate to your deposit, and the FX margin you see on the wallet side is layered on top of whatever the casino’s display-currency conversion was. The casino isn’t charging you a fee; they’re simply quoting prices in their working currency, and the cumulative effect for a GBP-banked player is non-trivial.

The honest summary is that UKGC casinos don’t charge you to deposit via Payz, and the operators take their compliance posture seriously. The all-in cost is still affected by mechanics that look operational rather than fee-shaped.

What Mastercard cash-out really costs

The Payz Mastercard is the route many players use to convert a wallet balance into spendable cash quickly, and it’s the route most often misunderstood from a cost standpoint. The card itself is straightforward — PSI-Pay’s Principal Member status with Mastercard since 2009 means the card is issued in-house rather than through an intermediary, which is why card-issuing in 173 countries and 44 currencies is feasible at PSI-Pay’s scale.

The cost layers on a Mastercard cash-out are: the loading fee from wallet to card (usually small or zero, depending on tier), the per-transaction limit and contactless cap on the card itself, the ATM withdrawal fee charged by the ATM operator (Payz doesn’t control this), and the FX margin if your card is loaded in a different currency than the country you’re using it in.

The transaction caps are the operationally important numbers. The Payz Mastercard’s maximum single contactless transaction in the UK sits at £100 or equivalent. Daily ATM cash withdrawals run up to €750-equivalent, and daily card purchases up to €5,500-equivalent. Those caps mean that if you’ve just won a meaningful sum and you want to convert it to cash via ATM, the card route doesn’t drain the balance in one visit — you’ll be doing multiple withdrawals across days, and each one of those withdrawals carries the ATM-operator fee separately.

Cross-currency Mastercard spending introduces a third layer. The card is loaded in your wallet’s currency. When you spend in a different currency, the conversion happens on the card-scheme side at a rate close to but not identical to mid-market, and the Payz tier margin applies. A Gold-tier user paying in GBP from a EUR-loaded card pays 1.49 per cent on the converted amount, plus whatever scheme-side rounding the day’s processing adds.

For a player using the card for occasional cash access — pulling £200 from an ATM after a successful weekend of play — the cost is modest and the convenience is real. For a player attempting to convert a large balance entirely through the card route, the daily caps slow you down and the cumulative ATM and scheme costs become a recognisable percentage of the withdrawal. The bank-transfer route is slower but usually cheaper for large amounts.

Three worked examples, end to end

The cleanest way to understand the all-in cost is to walk through it. Here are three end-to-end scenarios using realistic numbers, all in GBP for clarity.

Scenario one: the same-currency casual player. You hold Payz in GBP, you deposit £200 at a GBP casino once a month, you cash out roughly half of any winnings — say £100 a month. Your tier is Classic. FX charge: zero, because you never cross currencies. Wallet-side deposit fee: zero. Withdrawal-side fee: the Classic per-withdrawal charge on the bank route, applied to a £100 withdrawal. Over a year, your all-in wallet-side cost is essentially twelve small per-withdrawal fees. Total annual leakage: well under £50 in most realistic scenarios. This is what Payz costs a typical casual British player using GBP throughout.

Scenario two: the cross-currency volume player. You hold Payz in EUR — perhaps because you started using the wallet while living abroad, or because you keep EUR for cross-border purchases. You deposit the equivalent of £500 a month at a GBP casino. Your tier is Classic. The FX margin of 2.99 per cent applies on every deposit. Over twelve months you’ve moved £6,000 across currencies and paid roughly £180 in FX margin alone — before any withdrawal-side fees. At this volume, the Gold tier upgrade with its 1.49 per cent FX rate would have cost you the monthly maintenance fee but saved you about half of that £180. Net saving over a year: meaningful. The arithmetic is what makes Gold a rational choice for cross-currency users, and the same arithmetic is why a deeper look at when FX actually fires matters before you commit to a tier upgrade.

Scenario three: the post-win cash-out via Mastercard. You’ve won £800 net of wagering and you want it spendable. You move the balance onto your Payz Mastercard. Loading fee: minimal. You can’t pull the full £800 from a single ATM visit because of the daily ATM cap and the per-ATM-machine limits. You’ll do two or three ATM trips over two or three days. Each trip carries an ATM-operator fee — typically a few pounds — and a small Payz-side cost depending on tier. If the card is loaded in a currency that doesn’t match the ATM country, add the FX margin per withdrawal. Total all-in cost: low single-digit percentage of the withdrawal, in exchange for near-immediate cash access. If you’d routed via bank transfer instead, you’d have saved that percentage but waited one to three business days for the funds to clear.

The pattern across all three: same-currency play is essentially free, cross-currency play has a real and measurable cost that scales with the tier you sit on, and the Mastercard route is a convenience cost rather than a fee per se.

The five moves that actually cut your costs

Most fee-reduction advice for e-wallets is generic and unhelpful. The five moves below are the ones that actually shift the numbers for a UK player using Payz at a UKGC casino.

The first move is currency alignment. If you can hold a Payz GBP balance and deposit at GBP casinos, your FX cost is zero. The single biggest fee-reduction step is structural: stop crossing currencies at the wallet leg. For players whose wallet balance is in EUR for historical reasons, the right move is to consolidate into GBP gradually, eating one FX margin once rather than paying it on every deposit thereafter.

The second is tier-fit, not tier-climb. Upgrade only when your cross-currency volume justifies the monthly fee. Don’t upgrade to Gold because Gold sounds better; upgrade because the maths works. Run the calculation on your actual volume from the last six months.

The third is route selection on withdrawals. For large withdrawals, the bank-transfer route is cheaper. For small urgent cash needs, the Mastercard route is faster. Don’t default to one for both use cases. The clean test: if the withdrawal is more than five or six times the per-transaction bank fee, the bank route is almost always cheaper.

The fourth is dormancy avoidance. Either keep the wallet modestly active — one transaction per quarter is usually enough — or withdraw the balance out entirely when you’re done with a play period. PSI-Pay’s CEO Phil Davies has spoken about the firm’s compliance discipline, noting “we need to be crystal clear to prove that what our customers are providing is real and authentic” — the same discipline that makes the company sustainable also means dormancy fees exist as a real-cost recovery mechanism. The wallet won’t carry your balance for free indefinitely.

The fifth is reading the casino’s payment-method T&Cs before depositing, not after. The casino-side mechanics — bonus eligibility, wagering contribution, withdrawal-method tying — affect your all-in cost more than the wallet-side fee schedule does. Five minutes reading the operator’s payment-methods page beats a year of optimisation on tier choice.

The FCA’s own data on the e-money sector is a useful frame here. Among e-money firms that became insolvent between 2018 and 2023, the average shortfall in client funds was around 65 per cent. That figure is about provider selection, not fee minimisation — but the cheapest fee in the world is irrelevant if the wallet behind it carries unmanaged counterparty risk. Payz’s FCA registration and PSI-Pay’s regulatory record are the floor below which fee optimisation becomes pointless.

For a complete overview of trusted gambling platforms that accept this method, visit our guide to the best ecoPayz casinos in the UK.

Does the casino itself add any fee on top of Payz"s tier FX rate?

UKGC licensing conditions effectively prevent operators from charging direct deposit fees to consumers, so the cashier should display 0 per cent next to Payz on the deposit side. What casinos can and do affect, without it being a fee in the strict sense, includes bonus eligibility, wagering contribution rates from e-wallet-funded play, and withdrawal-method tying that may force a less-than-optimal cashout route. None of these adds a line item to your cashier display, but they affect the all-in cost of the deposit-to-cashout cycle.

How does the £100 contactless cap interact with Mastercard withdrawals from casino balances?

The £100 contactless transaction cap on the Payz Mastercard limits how much you can spend in a single tap, but it doesn"t cap the daily total. You can do multiple contactless transactions in a day up to the €5,500-equivalent daily purchase ceiling. For ATM cash-out, the relevant cap is the €750-equivalent daily ATM limit, which is independent of the contactless ceiling. A large withdrawal cashed out via the card route therefore takes multiple ATM visits across multiple days, not a single transaction.

Is the Gold-tier 1.49 per cent FX rate worth the monthly fee for an average UK casino player?

The break-even depends on your actual cross-currency volume. If your wallet balance and your casino"s display currency are the same, FX never fires and Gold"s monthly fee is pure cost — Classic is the right choice. If your annual cross-currency volume generates more in saved FX margin than Gold"s monthly fee costs over twelve months, the upgrade pays for itself. The clean test is to total your last twelve months of cross-currency deposits, multiply by 1.5 per cent (the gap between Classic and Gold), and compare to twelve times the monthly Gold fee. If the saved margin exceeds the annual fee, Gold makes sense.

Are e-money firms like PSI-Pay covered by the same protection as a UK bank account?

No — e-money safeguarding and bank-account protection are structurally different. Bank deposits up to £85,000 fall under the FSCS deposit guarantee scheme. E-money balances at FCA-authorised institutions like PSI-Pay (registration 900011) are protected under the EMRs safeguarding regime, which segregates client funds but doesn"t carry the same FSCS umbrella. Historic data on insolvent e-money firms shows average shortfalls of around 65 per cent in funds recovered to clients, which is the headline reason the FCA has been tightening the safeguarding regime under PS25/12.

ecoPayz Casino Articles: UK Market Trends and Payment Data

Published by the Ecopayz Casino UK team.