Payz Mastercard Casino Withdrawals: ATM Fees and UK Limits

Payz Mastercard: Hidden Utility for Casino Payouts

The Payz Mastercard tends to get described as an afterthought — “you can also order a physical card if you want one” — when in fact it’s the part of the Payz product that turns wallet winnings into actual spendable cash. I’ve had clients ignore the card for years, then suddenly realise that the friction of pulling a casino payout into their high-street bank account is exactly the friction the Mastercard removes. The card isn’t glamorous, but it’s quietly the most useful piece of the Payz toolkit for British players.

What's inside this guide

This piece is the practical guide I wish more people read before ordering the card. We’ll cover what the Mastercard actually is (it’s not what most players assume), the flow from casino payout to spendable cash, the daily and single-transaction limits that catch most users out, ATM fees and FX behaviour even when you’re standing in the UK, and the contactless ceiling that quietly governs in-person spending.

What the Payz Mastercard actually is

The Payz Mastercard is a prepaid Mastercard issued by PSI-Pay, the FCA-authorised e-money institution behind Payz. PSI-Pay has been a Mastercard Principal Member since 2009, which means it issues cards directly into the Mastercard scheme rather than through an intermediary bank. That’s an unusual position for a non-bank e-money firm and it matters for several practical reasons.

The card is funded from your Payz balance, not from a separate account. There’s no overdraft, no credit line, no chargeback-against-card-issuer in the same sense as a debit card from your bank. The Mastercard logo and the scheme membership give the card retail acceptance everywhere a Mastercard works, but the underlying account is your e-wallet, not a current account.

Physical and virtual versions exist. The physical card arrives by post and works at ATMs, in shops, online, and through contactless. The virtual card has no physical form — you get a number for online use, and it can be regenerated as a single-use number for privacy or fraud reduction. Both pull from the same Payz balance.

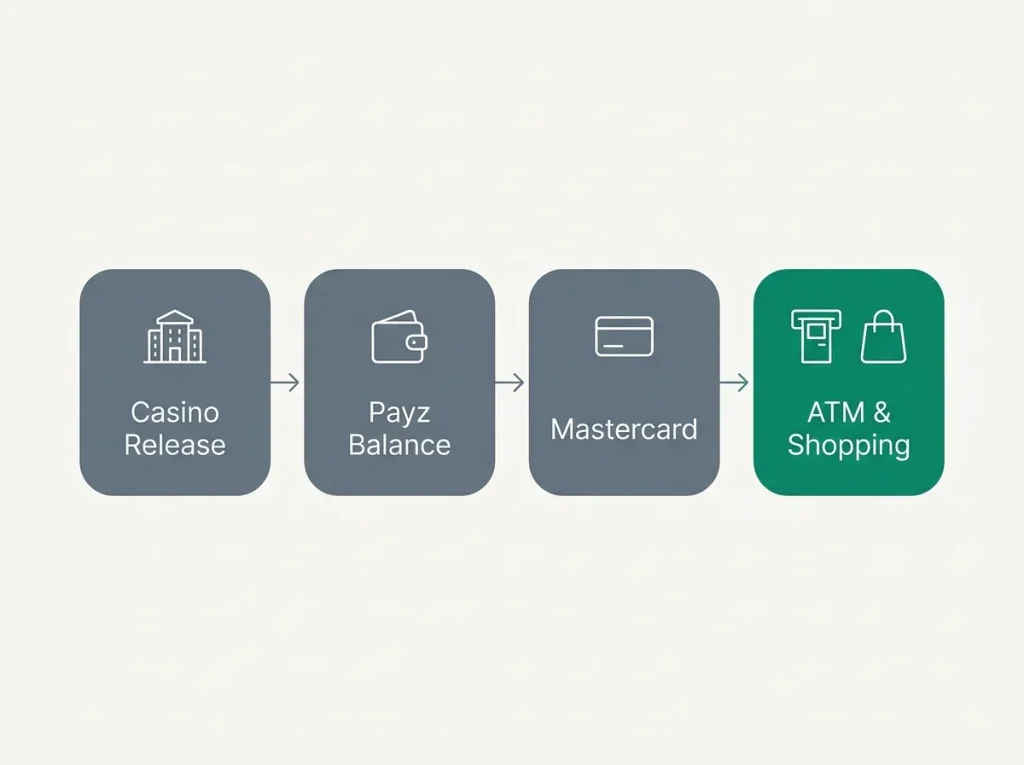

For casino-related use specifically, the card matters in one direction: turning Payz balance into spendable cash. Most casinos don’t accept the Payz Mastercard as a deposit method directly (they accept Payz the wallet), so the card’s role is downstream of the casino, not at the cashier.

The actual flow from casino payout to spendable cash

The shape of a Mastercard-routed withdrawal is straightforward once you’ve done it once.

The casino releases your winnings after its review. The funds land on your Payz balance, usually within an hour or two of the casino’s release. The Payz balance is now spendable through the Mastercard. You can use the card at a UK ATM to pull cash, in a high-street shop with contactless or chip-and-PIN, or online at any merchant that takes Mastercard. There’s no separate transfer step — the balance is the card’s funding source by default.

What this avoids: the days-long lag of pulling Payz balance into a UK bank account by Faster Payments. What it adds: ATM fees from foreign banks (more on those below), the contactless cap on in-person purchases, and the daily withdrawal limits that come with the tier you’re on.

PSI-Pay’s CEO, Andy Downes, framed the infrastructure underpinning the card plainly: “Our ability to successfully support a growing and developing solution over 20 years is testament to our agility, knowledge and ability to deliver.” That maturity shows up in card reliability — declines from technical issues are rare, and the card behaves consistently across UK and overseas use.

What sometimes catches new users out: the card is prepaid, so it has no credit cushion. If your Payz balance is £40 and you try to spend £45 on the card, the transaction declines. That’s by design.

The daily and single-transaction limits that catch people out

The limits vary by tier, and the tier you’re on shapes the card’s everyday usefulness more than the tier shapes the wallet itself.

Daily ATM cash withdrawals top out at up to €750 in the upper tiers — Gold and above. At Classic and Silver, the daily ATM ceiling is meaningfully lower. For a player trying to pull a £2,000 casino payout into cash over a few days, the daily ATM cap is usually the binding constraint, and the tier you’re on determines how many ATM visits the cash-out takes.

Daily purchase limits top out at up to €5,500 in the upper tiers. That’s high enough to handle most real-world expenses — a hotel bill, a flight, a piece of electronics — without re-tiering or splitting transactions. At lower tiers, the daily purchase cap is tighter, and splitting larger purchases across days becomes the workaround.

Single-transaction limits exist alongside daily limits, and they sometimes catch users out. A large single purchase that fits inside the daily cap can still be declined if it exceeds the single-transaction ceiling. That’s most likely to happen on Classic at single-shop totals above a few hundred pounds.

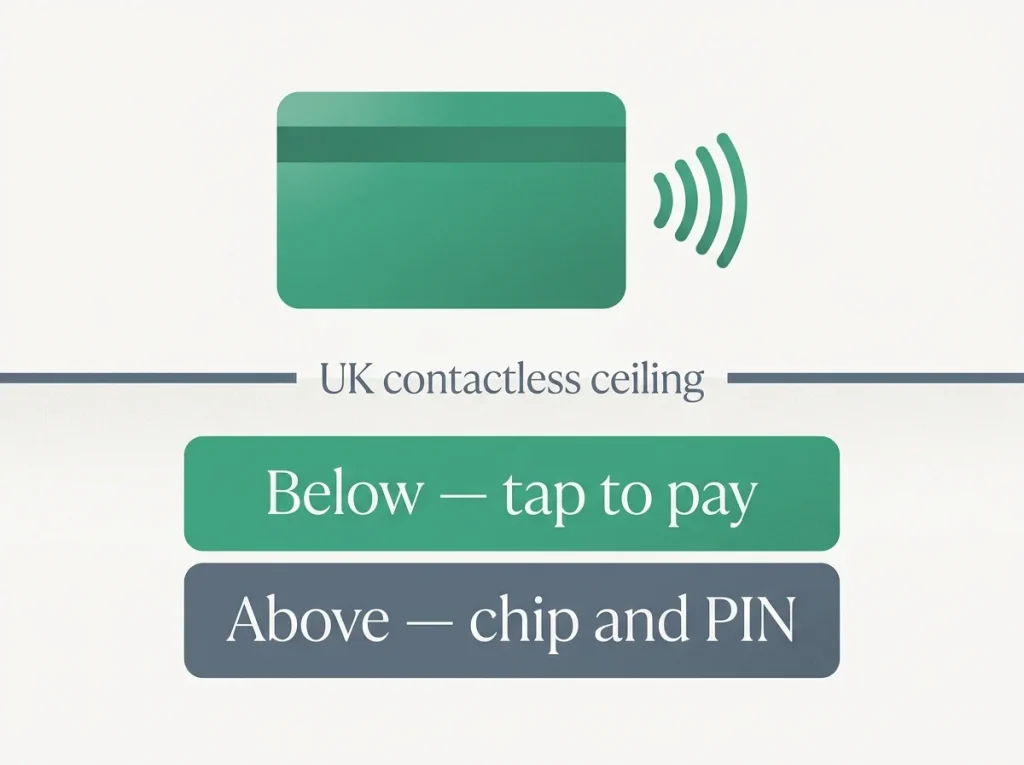

The contactless ceiling — the single biggest limit most players actually encounter — sits at £100 per transaction in the UK across every tier. Tier doesn’t lift it because it’s a Mastercard scheme rule, not a Payz setting. For anything over £100 in person, you need chip-and-PIN.

ATM fees and FX behaviour, even at UK ATMs

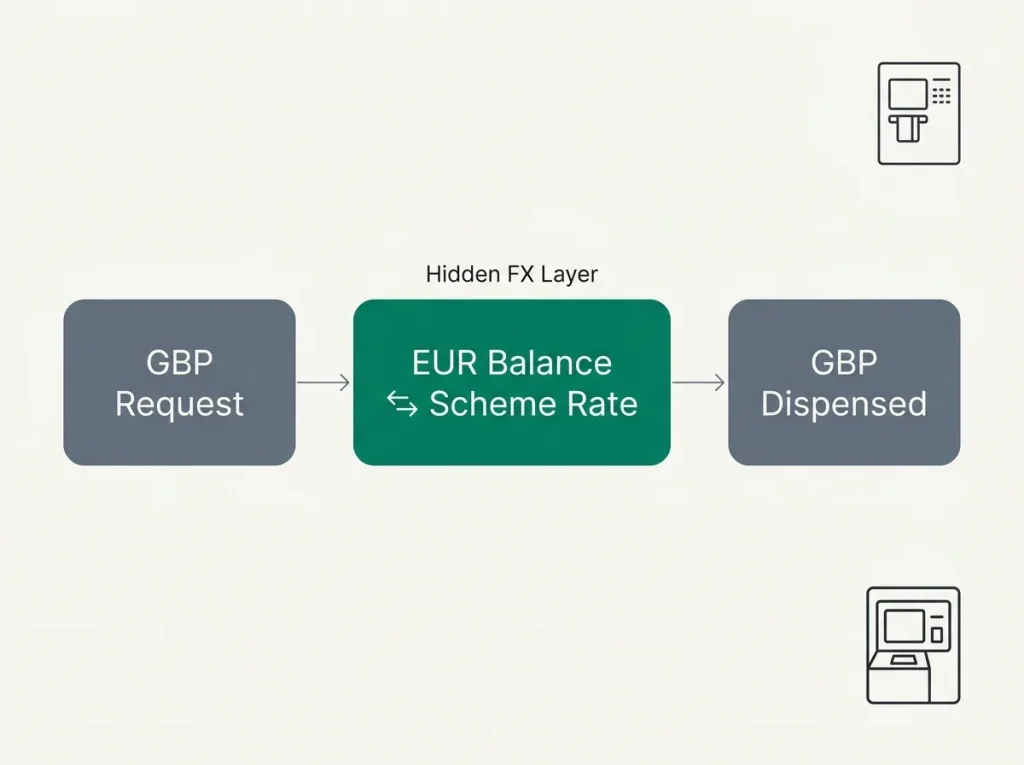

This is the section that confuses more first-time card users than any other. The Payz Mastercard is a euro-denominated card by default, which means an ATM withdrawal in pounds at a UK ATM triggers a euro-to-pound conversion behind the scenes, even though you’re standing in Britain.

The mechanics: the card carries a balance that’s been settled in euros (with your Payz wallet doing the GBP-to-EUR conversion when the balance loaded), and the UK ATM withdrawal asks for pounds. The ATM communicates with the Mastercard scheme, which converts the euro balance to pounds at the scheme rate plus PSI-Pay’s tier FX rate. You end up paying conversion fees both directions if your wallet balance started in GBP.

The way to avoid this: hold the Payz balance in pounds (open a GBP sub-account inside Payz), and use a Payz GBP-issued card if available, or accept the FX layer and pick the cheapest tier you can. The card was originally designed for international cross-border use, where the multi-currency nature is a feature. In single-country UK use, it sometimes acts as a friction.

ATM fees on top of the FX: the operator of the ATM may charge its own fee, especially at non-bank ATMs (the standalone kiosks in pubs and convenience stores). PSI-Pay doesn’t control that fee. Sticking to bank-operated ATMs at the major high-street chains usually keeps that fee at zero.

Contactless and online purchases, in practice

Contactless behaves like any other Mastercard contactless card in the UK, capped at £100 per transaction. Above that, you’ll need to insert the card and enter your PIN. The £100 ceiling is a UK-wide Mastercard scheme rule, not a Payz-specific one.

Online purchases work normally. The card details — number, expiry, CVV — can be entered at any Mastercard-accepting merchant. 3D Secure prompts route through the Payz app, so make sure the app is set up with notifications enabled. Single-use virtual card numbers can be generated for high-risk merchants, giving a layer of privacy and one-shot fraud protection.

Adding the Payz Mastercard to Apple Pay or Google Wallet works for most users — the card number tokenises into the mobile wallet the same way any debit card would. From there, you can tap to pay with your phone. The contactless ceiling still applies.

For day-to-day casino-related use, the card flow is typically: casino payout into Payz balance, Payz balance is spendable through the card. That’s it. The simplicity is the point, and the path from casino to card is part of the wider withdrawal mechanics covered in my complete guide to ecoPayz casino withdrawals.

Why does my ATM withdrawal in GBP still trigger an FX conversion when I"m in the UK?

The Payz Mastercard is built on a euro-denominated base by default. Even at a UK ATM dispensing pounds, the underlying conversion runs through your Payz balance and the Mastercard scheme rate plus your tier FX. Holding a GBP sub-account inside Payz before using the card is the simplest fix — that way the balance source matches the withdrawal currency and the FX layer doesn"t activate.

Can the Payz Mastercard be added to Apple Pay or Google Wallet for casino-related purchases?

Yes, for most users. The card number tokenises into Apple Pay or Google Wallet the same way a normal debit card does. Once added, you can tap to pay with your phone at any contactless merchant, subject to the standard £100 contactless ceiling. The card isn"t typically usable to deposit at a UK casino directly — most casinos accept Payz the wallet, not the card.

ecoPayz Casino Articles: UK Market Trends and Payment Data

Prepared by the Ecopayz Casino UK editorial staff.