ecoPayz vs PayPal: Compare UK Casino Transaction Fees

PayPal vs ecoPayz: Evaluating Market Penetration and Fees

The first time I sat across from a Brighton client trying to decide between Payz and PayPal for his weekly slot habit, he had already lost two welcome bonuses to e-wallet exclusion clauses he hadn’t read. That was 2021. The wallets have shifted since then — Payz finished its rebrand from ecoPayz, and PayPal quietly tightened gambling availability across half of UKGC’s licensee list — but the same decision still sits in front of every British player every weekend.

What's inside this guide

This isn’t a contest one side wins outright. PayPal carries the mainstream payments halo and a chargeback culture built into Mastercard and Visa schemes. Payz carries lower FX rates, broader casino acceptance for international rails and an FCA authorisation that few players ever look up. The interesting question isn’t which is better — it’s which one costs you less in the way you actually deposit and withdraw. With 57% of UK adults now registered for a mobile wallet, up sharply from 42% a year earlier, the choice has stopped being academic.

Where each wallet actually shows up at UK casinos

Walk into a UK casino cashier and you’ll notice something odd in the e-wallet drawer. Payz often sits alongside Skrill and Neteller as a near-default trio. PayPal turns up much more sparsely — and when it does, it’s usually at the bigger, FTSE-listed brands. I keep an internal acceptance list for both, and the gap is wider than most players assume.

The reason is structural. PayPal lets each merchant categorise its own UK presence, and many UKGC operators either don’t qualify under PayPal’s risk filter or don’t want to absorb the higher per-transaction cost. Payz comes from a different lineage. PSI-Pay, the UK e-money institution behind it, sits third in the e-wallet category for online gambling globally, behind Neteller and Skrill but ahead of every other consumer brand. That positioning means Payz integrations are built into casino payment stacks by default at most platforms.

What you’ll see in practice: Payz available at roughly four out of five UKGC-licensed casinos I check; PayPal at maybe one in three. The split is most extreme at newer, smaller-budget operators, where PayPal is rare and Payz is standard. At the top ten brand-name British casinos, both usually appear, and the choice falls back to fees and bonus eligibility — the two sections that follow.

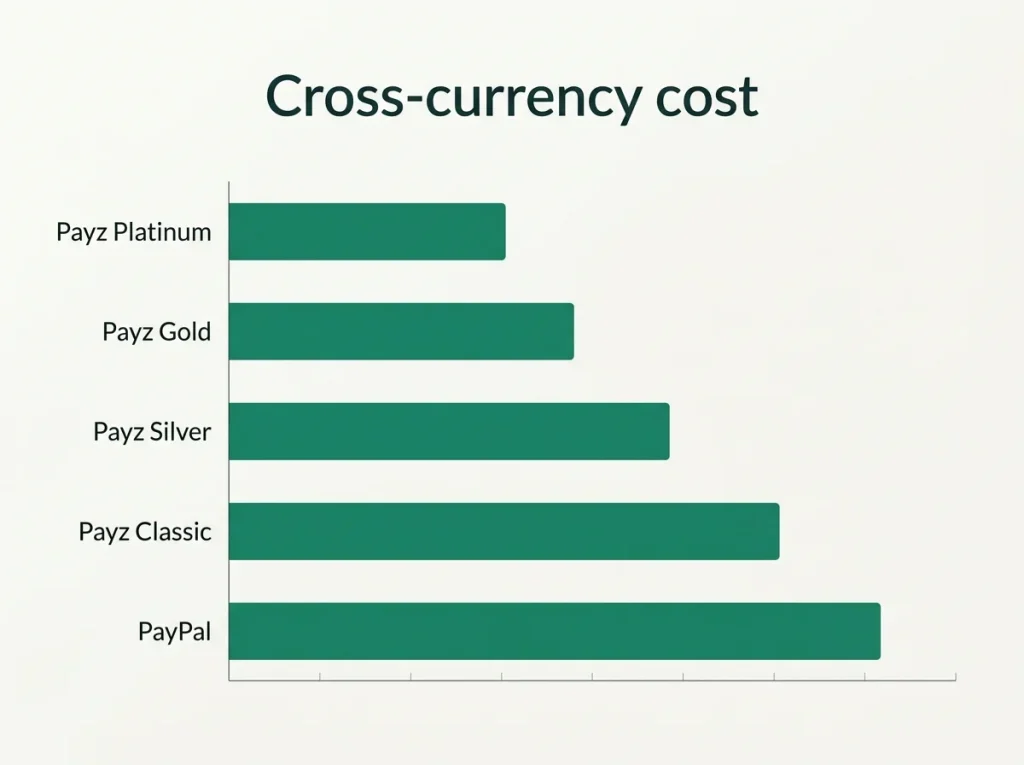

Fee comparison from deposit to FX

PayPal feels free until you read the small print on cross-border charges. Payz feels cheap until you compare it against your own tier’s FX rate. I rebuild this comparison every quarter for clients, and the same pattern keeps emerging: the headline numbers mislead in opposite directions.

PayPal in the UK charges no consumer fee for sterling-to-sterling deposits at most casinos. The cost is bundled into what the merchant pays. Cross-currency transactions are a different story. PayPal’s currency-conversion margin on personal transactions sits around 3 to 4 percent above mid-market, and that margin applies whenever the casino settles in any currency other than the one your PayPal balance happens to hold.

Payz takes a more transparent route: a tier-based FX rate published openly on its fees page. Classic and Silver tiers both run a 2.99% FX rate. Gold drops it to 1.49%. Platinum and True VIP land at 1.25%. There is no per-transaction deposit fee on the Payz side for funding a UK casino balance — the FX rate is the entire embedded cost when currencies differ. If your balance is already in GBP and the casino debits in GBP, there is no FX at all. A clean zero on the wallet side.

Where PayPal can edge ahead: pure GBP-to-GBP, with no chargeback claim ever expected, the comparison is roughly a wash, with PayPal’s bundled merchant pricing often invisible to the player. Where Payz wins quietly: any deposit that touches a foreign-currency casino balance, any deposit on Gold tier or above, and any high-volume monthly pattern where the lower marginal FX rate compounds. For a £400-a-month UK casino player who occasionally uses Curaçao-headquartered platforms, the saving I usually see lands somewhere between £8 and £15 a month — not dramatic per deposit, real over a year.

Bonus eligibility and promo rules

The exclusion clause is the gotcha that catches almost every new e-wallet user. I keep a screen-grab folder of UK casino terms specifically for the “e-wallet deposits not eligible for welcome bonus” line. The exact wording varies, but the effect is identical: deposits from Payz and PayPal both trigger the clause at most operators.

Why both? Operators built that filter around 2017 to 2019, when bonus-hunters routinely used e-wallets to deposit, claim, wager the minimum and withdraw before contributing meaningfully to revenue. The casino doesn’t really distinguish between Payz and PayPal in that filter. It groups e-wallets as a category and excludes the whole group, sometimes alongside prepaid cards.

There is a thinner tier of UK operators that does allow e-wallet bonuses — typically smaller platforms still trying to win market share, with stricter wagering on the bonus itself. At those sites the rule is symmetric: if PayPal qualifies, Payz qualifies; if one is blocked, both usually are. The exception is reload offers, where I see a slightly higher allowance for both wallets than on the welcome. That’s probably because reloads come from already-verified customers, who carry less bonus-abuse risk.

If a welcome bonus matters to you, the deposit method needs to come second after reading the terms and conditions. Both wallets sit on the wrong side of that fence at most British casinos.

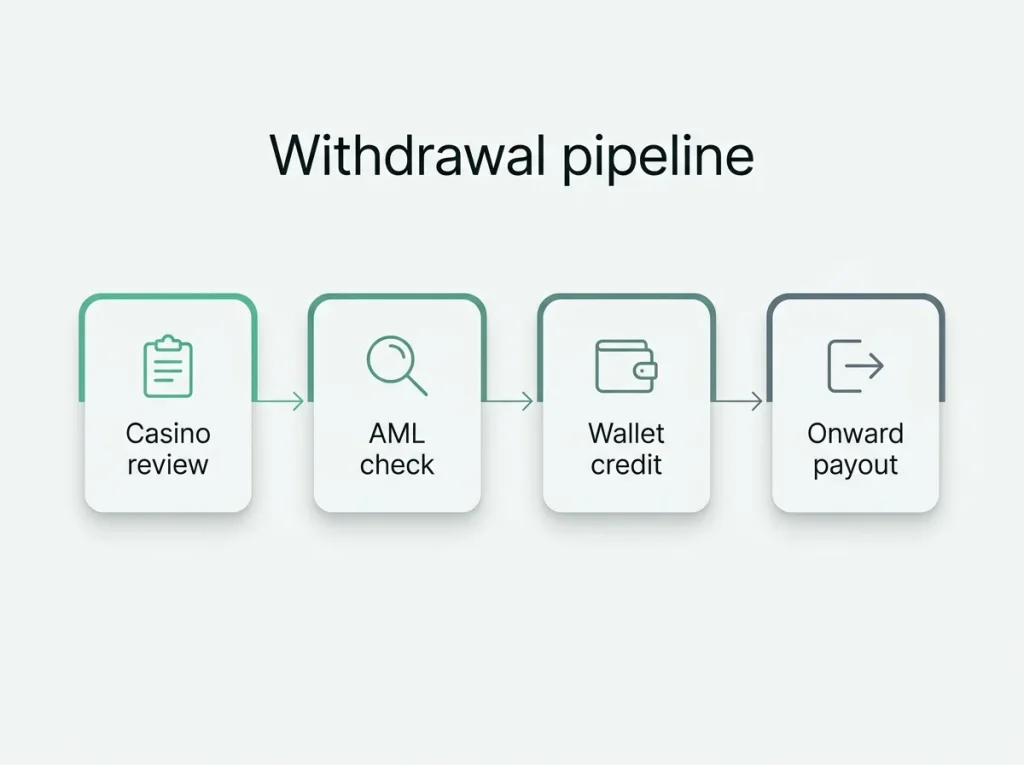

Withdrawal speed and the limit ceiling

Both wallets pitch themselves as fast. Both deliver — once the casino has finished its own review. The withdrawal speed gap is real but smaller than the marketing suggests, and it sits in a different part of the pipeline than most players assume.

Casino-side review consumes the first six to forty-eight hours of any withdrawal, regardless of wallet. That clock is set by the operator’s AML and social responsibility controls, and every UKGC licensee has tightened these after a wave of enforcement actions in 2025. PayPal and Payz don’t influence this stage at all.

Once the casino releases the funds, the wallet stage diverges. PayPal commonly credits within minutes for sterling balances. Payz typically credits to the Payz balance inside the first hour, sometimes immediately. If you then push the Payz balance to a Mastercard payout, that adds another business day. PayPal’s onward flow to a UK bank account adds one to three days unless you pay for the instant transfer feature.

Limit ceilings are where the difference becomes structural. PayPal applies per-transaction limits that vary by verification status and merchant category, and the gambling category attracts tighter caps than retail. Payz uses its tier system — Classic limits are tight, Gold and above open the room considerably. For a single-digit-thousand withdrawal, both work. For five-digit cashouts, Platinum-tier Payz usually has more headroom in a single cycle than a verified UK PayPal account.

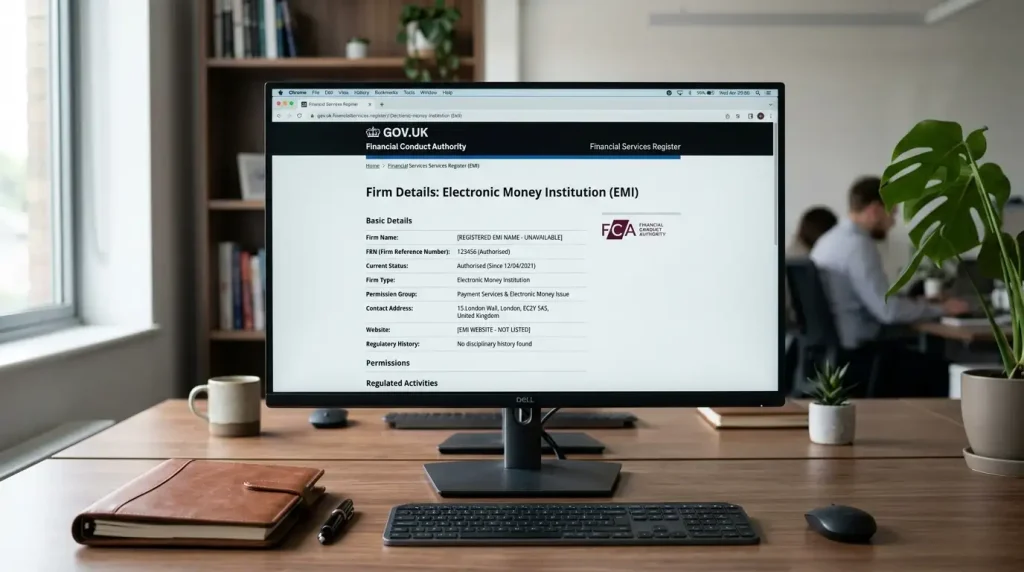

Safety, FCA and Mastercard scheme cover

People assume PayPal is the safer pick because the brand is older and the chargeback culture is louder. The regulatory reality is more even. PayPal (Europe) operates as a Luxembourg-licensed bank under CSSF supervision. PSI-Pay Limited, the company behind Payz, sits on the FCA register at number 900011 as an Authorised e-Money Institution.

Both are regulated. Neither is a UK retail bank. Both segregate client funds under their respective safeguarding rules — PSI-Pay under the UK Electronic Money Regulations 2011 and the new FCA Policy Statement PS25/12 taking effect on 7 May 2026, PayPal under Luxembourg equivalents.

Chargeback rights only apply if the underlying funding instrument is a card scheme. A debit-card-to-PayPal-to-casino chain preserves a thin chargeback claim against the card issuer. A Payz top-up from your bank by Faster Payments leaves no equivalent chargeback path. That’s the substantive safety asymmetry worth knowing — PayPal preserves more downstream consumer-rights infrastructure when the underlying funding is a card. For everything else — fraud protection, account access controls, two-factor authentication — the two are functionally similar.

A profile-by-profile pick

There is no general winner here. Each wallet fits a profile, and the choice gets cleaner once the profile is named.

Pick PayPal if your casino spend is concentrated at one or two FTSE-name UK operators, you deposit and withdraw in pounds only, you fund from a debit card you’d want a chargeback path on, and you don’t care about welcome bonuses on e-wallets. The premium for those qualities is small.

Pick Payz if you play across more than three brands, including any platform headquartered outside the UK, your deposits average more than £200 monthly, you’ve already worked your tier up to Silver or Gold, or you value an explicit fee table over PayPal’s bundled merchant pricing. The compounding fee saving and the broader casino acceptance both quietly pay off.

The hybrid pick — Payz for the bulk of activity, PayPal kept warm for the one or two casinos where it qualifies for offers — is what I end up recommending most often. Each wallet’s strength is concentrated enough that picking only one closes off too much. A multi-rail setup, which complements the difference between an e-wallet and a Pay-by-Bank rail covered in my comparison of Payz against Trustly, has become the British casino player’s default in 2026.

Why is PayPal accepted at fewer UK casinos than Payz despite being more mainstream?

PayPal applies its own risk filters to gambling merchants, and many UKGC licensees either don"t qualify or refuse the higher per-transaction cost. Payz, through PSI-Pay, was built into casino payment stacks as a gambling-friendly e-wallet from the start, which gives it default-on placement at most operators.

Do UK casinos block welcome bonuses for both Payz and PayPal users equally?

Most UKGC operators apply a single e-wallet exclusion clause that covers both wallets alongside Skrill and Neteller. The smaller subset of casinos that does allow e-wallet bonuses usually treats Payz and PayPal symmetrically — either both qualify or both don"t, with the same wagering rules on whichever is allowed.

ecoPayz Casino Articles: UK Market Trends and Payment Data

Prepared by the Ecopayz Casino UK editorial staff.