ecoVoucher UK Casinos: Prepaid Payz Top-Up Codes

ecoVoucher Utility: Offline Cash for Online Casino Deposits

I had a client last year — a retired teacher in Bristol — who specifically wanted to keep her casino spending entirely off her bank statement. Not for any guilty reason; she just liked the discipline of a ring-fenced budget. ecoVoucher solved her problem in a way nothing else inside the Payz ecosystem could. She bought vouchers with cash at a high-street agent, redeemed them into her Payz balance, and her current account never saw a single gambling-adjacent transaction. That’s the use case ecoVoucher was built for, and it’s narrower than the marketing suggests.

What's inside this guide

This piece walks through what ecoVoucher actually is inside the Payz product family, where to buy them in Britain, how the redemption flow works, which UK casinos respond well to voucher-funded balances, and the AML controls that have tightened around prepaid voucher methods through 2025 and 2026. With 57% of UK adults now registered for a mobile wallet, the appetite for cash-to-digital bridges remains real — and ecoVoucher is one of the cleaner ones still operating.

What ecoVoucher is inside the Payz ecosystem

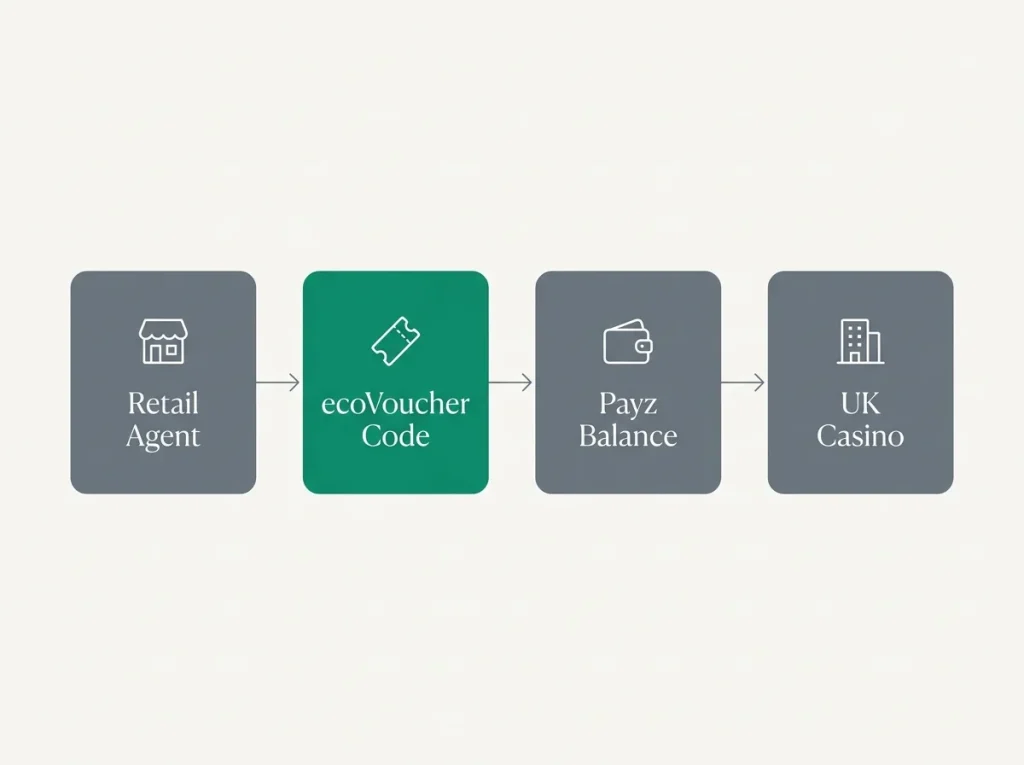

ecoVoucher is a prepaid top-up code that loads value into a Payz balance. It is not a casino payment method in its own right at UK casinos — you can’t go to a cashier and pay with a voucher directly at most operators. It’s a step that sits upstream of the Payz wallet: cash or card buys a voucher; the voucher redeems into Payz; Payz then funds the casino deposit.

The voucher is issued by partners in the Payz network. Each voucher carries a unique 16 to 19 digit redemption code and a fixed face value (typically in £10 increments up to £150 for smaller vouchers, with higher denominations available at some agents). The code is valid for one redemption only — once entered into a Payz account, it’s spent and the balance increase is irreversible.

PSI-Pay, the FCA-authorised e-money institution behind Payz (FCA register number 900011), treats ecoVoucher as a regulated top-up method subject to the same anti-money-laundering controls as any other inbound funding source. The light-touch nature of the cash purchase doesn’t translate into light-touch handling once the value enters the Payz ecosystem.

For UK casino players, the practical role of ecoVoucher is a privacy bridge — turning cash or card payments at a non-gambling retail agent into spendable Payz balance, with no gambling-related entry on the buyer’s bank statement.

How to actually buy an ecoVoucher in Britain

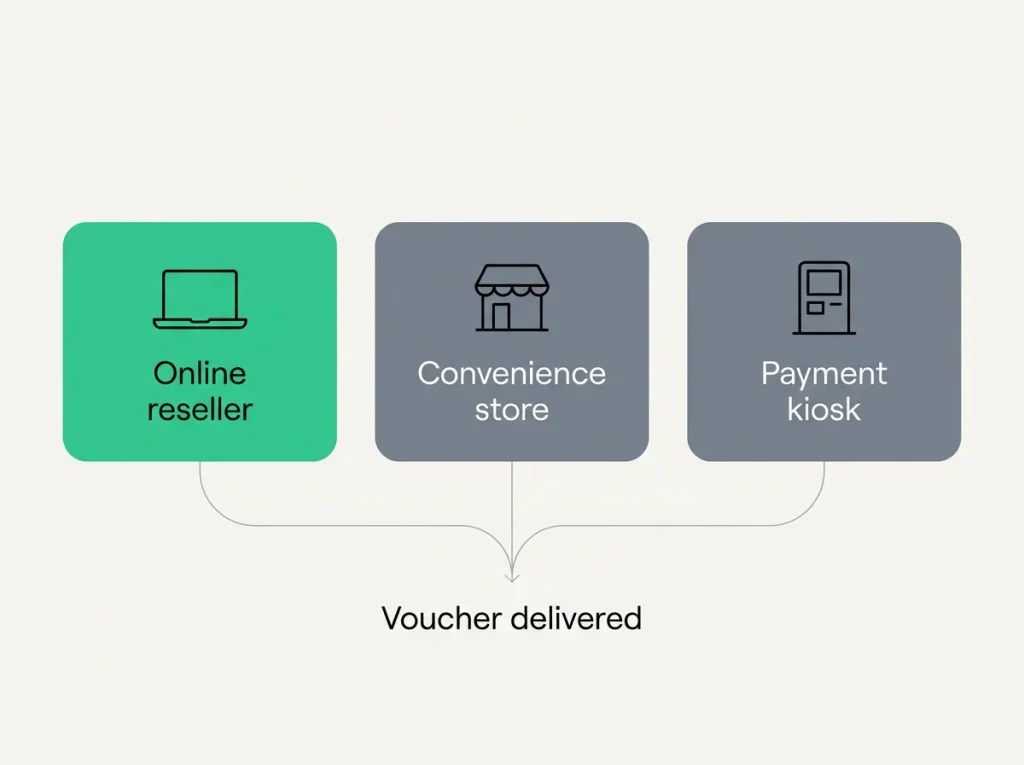

The British availability of ecoVoucher has thinned over the past few years compared to mainland Europe, where the voucher network is denser. In 2026, the realistic options for UK residents are: online resellers that accept card payment for a voucher delivered by email, a smaller set of physical retail agents (some convenience stores, kiosks and select payment shops), and authorised partners in the Payz/PSI-Pay extended network.

Online purchase is the most common route. A reseller’s website takes a card payment, processes the order, and delivers the voucher code by email within minutes. The card payment shows up on your bank statement as a payment to the reseller — not to a casino, not to a gambling brand — which is the privacy gain compared to a direct casino deposit.

Physical purchase is patchier. The retail agent footprint depends heavily on your region. London and the larger cities have more options; rural areas have fewer. Where physical agents exist, they typically accept cash, card and sometimes contactless. Cash-purchased vouchers are the only fully off-statement route, and they’re the option that triggers the most AML scrutiny downstream.

Voucher denominations vary by region and agent. The most common UK denominations are £10, £25, £50, £75 and £100, with £150 sometimes available. Multiple vouchers can be combined to fund larger deposits.

Redeeming a voucher into a Payz balance

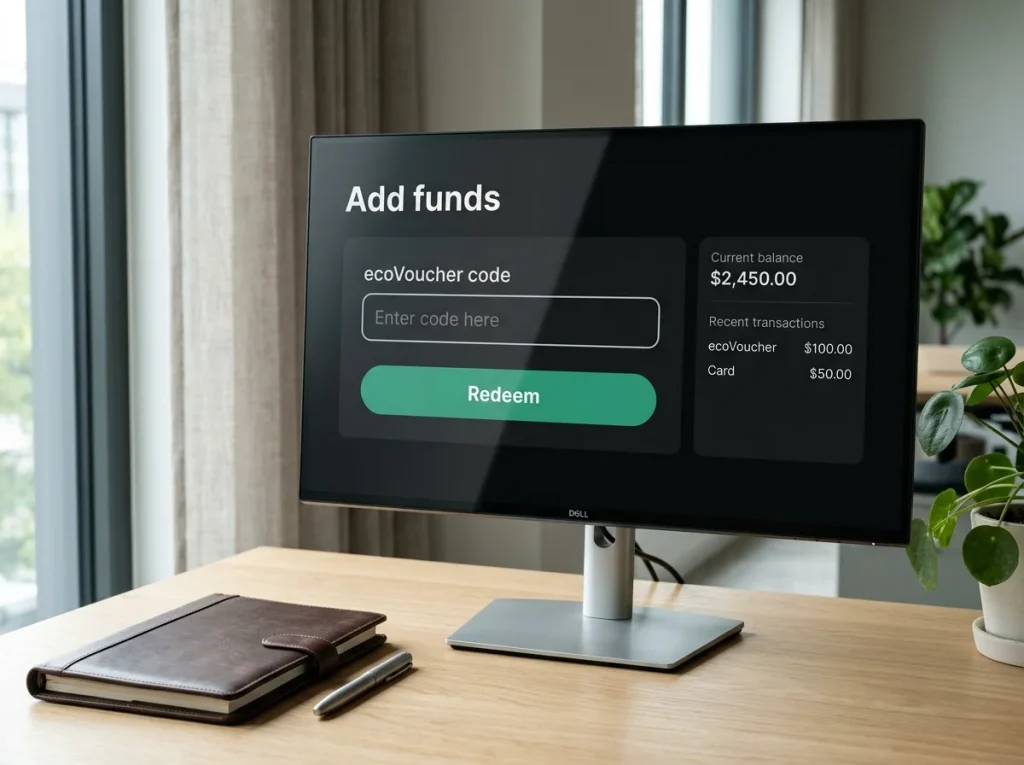

Redemption is straightforward and fast in most cases.

You log into your Payz account (web or app), navigate to the “add funds” or “deposit” section, choose ecoVoucher as the funding method, and enter the voucher code. The system verifies the code’s validity, debits it against the voucher network’s records, and credits your Payz balance with the equivalent value. The whole flow takes under two minutes when nothing goes wrong.

What can go wrong: a code that’s been entered with a digit error returns an error message. A code that’s already been redeemed elsewhere returns a “voucher used” message. A code from an expired voucher batch — vouchers have an expiry date printed on them — returns an “expired” message. In all three cases, the voucher cannot be refunded after the fact, so triple-checking the code at entry is worthwhile.

An FX layer activates if the voucher denomination is in a different currency from your Payz wallet base currency. A EUR voucher redeemed into a GBP-based Payz balance triggers a conversion at your tier rate (2.99% at Classic and Silver, 1.49% at Gold, 1.25% at Platinum and True VIP). Buying GBP vouchers into a GBP Payz balance avoids this.

Once redeemed, the value behaves exactly like any other Payz balance — spendable at casinos, withdrawable to the Payz Mastercard, transferable subject to tier limits.

How UK casinos respond to voucher-funded Payz balances

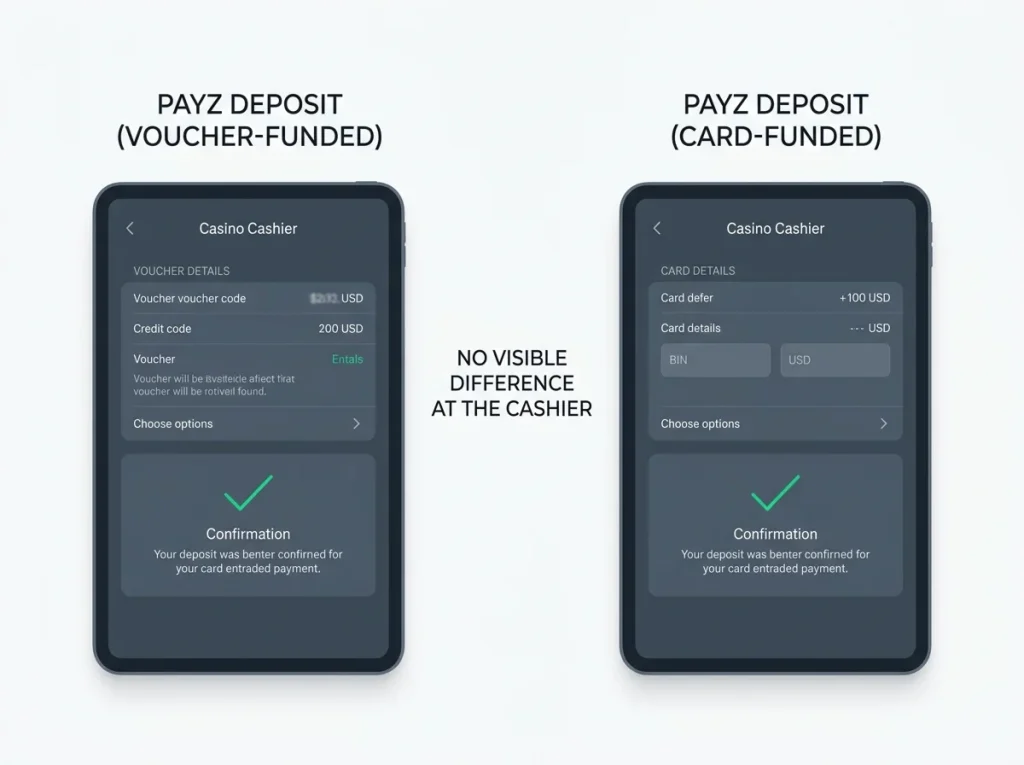

Here’s the subtle point most voucher users don’t realise: the casino doesn’t know how your Payz balance was funded. From the cashier’s perspective, a Payz deposit funded by ecoVoucher looks identical to a Payz deposit funded by a bank transfer or card top-up. The voucher provenance is invisible at the casino end.

That said, the casino’s KYC stack still applies. The casino sees you, your registered address, your identity documents — everything it would see for any Payz user. Voucher funding doesn’t make the casino account anonymous. It just keeps the funding step off your bank statement.

Where voucher funding can matter at the casino: bonus eligibility. Some operators that allow Payz for general play still exclude voucher-funded balances from welcome bonuses on the grounds that vouchers are harder to source-verify. The exclusion is rare but real, and it usually appears in the bonus terms rather than the general payment-method list. Reading the bonus T&Cs before depositing is the only way to spot it.

Withdrawal-wise, money paid out of a casino into a voucher-funded Payz balance behaves identically to money paid out into any other Payz balance. The voucher origin of the funds doesn’t affect withdrawal speed, limits or KYC.

The AML controls now wrapped around prepaid vouchers

The UKGC has been visibly tightening enforcement around prepaid vouchers as a category through 2025. The clearest example: Videoslots Limited was fined £650,000 in November 2025 for AML and social responsibility failures that included, in the regulator’s published findings, the use of pre-paid digital vouchers for gambling without effective oversight. That case shifted the industry baseline.

What this means in practice for ecoVoucher users in 2026: expect tighter casino-side scrutiny on any account where voucher-funded Payz deposits account for the majority of activity, especially at higher volumes. Source-of-funds requests come earlier in the customer lifecycle. Documentary thresholds are tighter. Withdrawals on flagged accounts can sit longer in pending review.

PSI-Pay applies its own AML controls at the voucher-redemption step. High-value redemptions trigger automated checks; recurring redemption patterns from new accounts attract human review. Vouchers purchased entirely in cash, in particular, sit higher on the risk-engine attention list than card-purchased ones.

For most British casino players, the practical effect is small — modest voucher use blends into normal Payz activity. For users whose entire casino budget is voucher-funded, the friction is noticeably higher than it would have been in 2023. The alternative privacy route inside the Payz product family — the virtual card — is covered in my guide to the Payz virtual Mastercard for casinos, and it’s worth weighing against ecoVoucher before committing to one privacy strategy.

Can I deposit an ecoVoucher directly at a UK casino, or must I top up Payz first?

At nearly every UK casino, you must redeem the voucher into your Payz balance first, then deposit from Payz. Direct voucher deposit at the cashier is not a standard option at UKGC-licensed operators. The voucher"s role is to fund the wallet, not to act as a casino payment method in its own right.

Are ecoVouchers anonymous from the casino"s KYC perspective?

No. The casino still runs its own KYC on you regardless of how your Payz balance was funded. What the voucher does is keep the funding step off your bank statement. The casino account itself stays linked to your verified identity, address and (often) source-of-funds documentation.

ecoPayz Casino Articles: UK Market Trends and Payment Data

Published by the Ecopayz Casino UK team.