ecoPayz vs Apple Pay: UK Casino Transaction Comparison

Payment Category Differences: Avoiding Unnecessary Transaction Fees

A friend of mine asked me last winter why his Apple Pay deposit at a British casino just got dismissed as “card payment” in his iPhone statement, while his Payz deposits showed up as proper e-wallet transactions. He’d been treating both as the same kind of thing for two years. They aren’t. The cashier groups them the same way the cinema groups popcorn sizes — visually parallel, structurally different.

What's inside this guide

Apple Pay is a tokenisation layer on top of your existing debit or credit card. Payz is a standalone e-money account holding a balance separate from any card. The shift to mobile-first payments is real — 57% of UK adults are now registered for a mobile wallet, and 25% of people aged 65 and over now use them, up from 14% only a year earlier. Adrian Buckle at UK Finance put it bluntly: “2024 was a year of firsts, all pointing to the growing shift towards digital payments.” But “mobile wallet” is a category that hides two very different beasts, and at the cashier they behave nothing alike.

What each actually is, under the surface

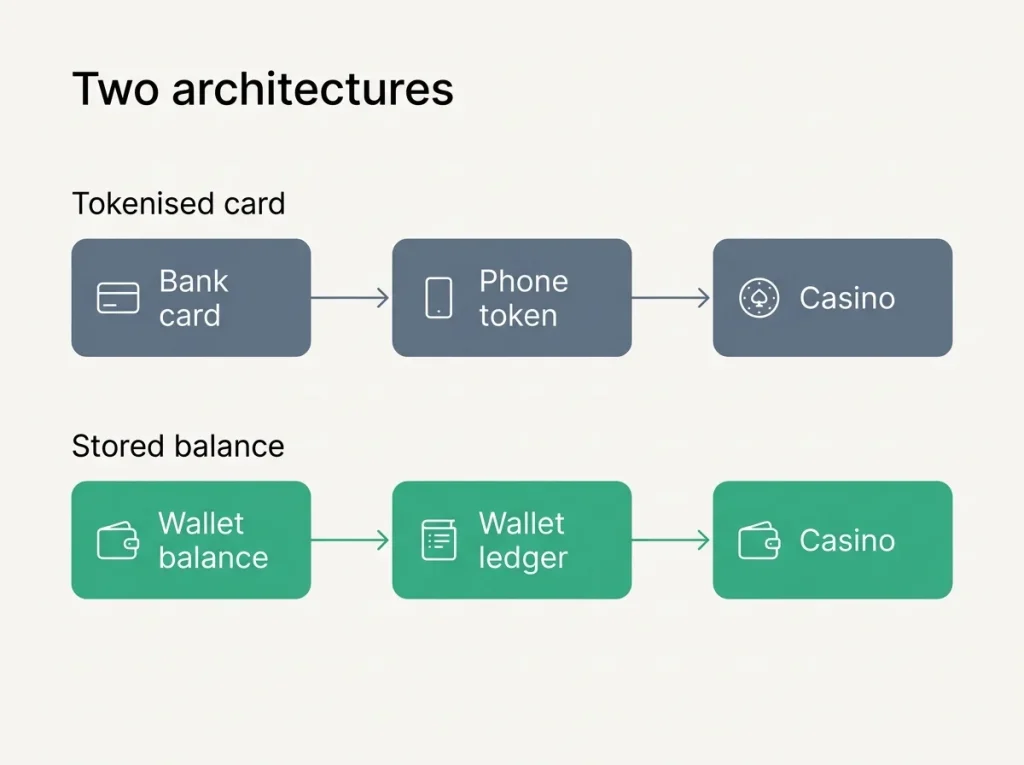

Strip the marketing away and the difference becomes obvious. Apple Pay is a wrapper. Payz is a wallet.

Apple Pay does not hold money. When you tap your iPhone or Apple Watch, it sends a tokenised version of your underlying card number to the merchant. That token is good for one transaction and then expires. The bank that issued the underlying card is the one debiting your account. From the casino’s perspective, an Apple Pay deposit is functionally a card payment routed through an extra security layer. The merchant category, the fee structure, the consumer rights — all inherit from the underlying card.

Payz is the opposite. PSI-Pay, the FCA-authorised e-money institution that runs it, holds your money in a safeguarded account on its books. When you spend Payz at a casino, the casino is debiting that balance directly. There’s no card involved unless you choose to use the optional Payz Mastercard for a withdrawal. The underlying source of funds — your bank, a top-up card — affects only how the balance was created, not how the casino sees the payment.

One is a sleeker way to swipe a card. The other is a separate financial account with its own regulator file number. Mixing them up costs money in fees, friction and bonus eligibility, in that order.

The funding-source question that decides everything

If you ask “where does the money come from?”, Apple Pay and Payz answer with the same vague gesture toward the user. The accurate answer is buried two layers deep.

Apple Pay’s funding source is whatever card you’ve loaded into the wallet — a Barclays debit card, a Monzo card, a Mastercard from your high-street bank. Every Apple Pay transaction passes through that card’s rails. If your card has a daily limit, Apple Pay inherits it. If your bank blocks gambling categories — and many UK banks now offer that toggle — Apple Pay deposits are blocked too. Around 18.9 billion of the 26.1 billion UK debit card payments in 2024 were contactless, and a chunk of those flowed through Apple Pay or Google Wallet on a phone.

Payz’s funding source is layered. You fund the Payz balance once (by card, bank transfer or voucher), and then you spend that balance multiple times at casinos. The casino doesn’t see your underlying funding source — only the Payz balance. That separation matters when you want to keep gambling activity off your main bank statement, or when your bank’s gambling block would otherwise stop a transaction.

For players who like the discipline of “I fund a casino budget once a month and then play within it”, Payz’s architecture matches the intent. For players who prefer the transparency of “every spend hits my bank account immediately”, Apple Pay matches better.

Casino acceptance rates in 2026

The gap is wider than I expected when I started tracking it. Apple Pay’s growth in UK retail has been enormous — yet at British casinos, it sits well behind Payz in acceptance.

Payz turns up at roughly four out of five UKGC-licensed casinos in my acceptance log. Apple Pay turns up at perhaps two out of five, concentrated at the larger brand-name operators that have integrated the relevant payment processor. The reasons are technical and regulatory. Apple Pay requires the casino’s payment processor to support the Apple Pay merchant ID flow, which not every processor does. Payz, through PSI-Pay, has been a built-in option in casino payment stacks for over a decade.

The age effect is real too. Apple Pay’s surge among 65+ adults — that jump from 14% to 25% in a year — has shifted the casino acceptance map. Some operators added Apple Pay specifically to serve older players who’d struggled with e-wallet sign-ups. For a player whose phone already has Apple Pay set up, the temptation to use it at the cashier is obvious. The narrowness of acceptance is the catch.

Fees and limits compared

Apple Pay charges no fee to the consumer. The cost is bundled into the underlying card’s interchange rate, which the merchant absorbs. There is no FX layer in Apple Pay itself — currency conversion, if any, happens inside the card-issuer’s rails. Limits are inherited from the card: daily contactless caps, online purchase ceilings, gambling-category blocks.

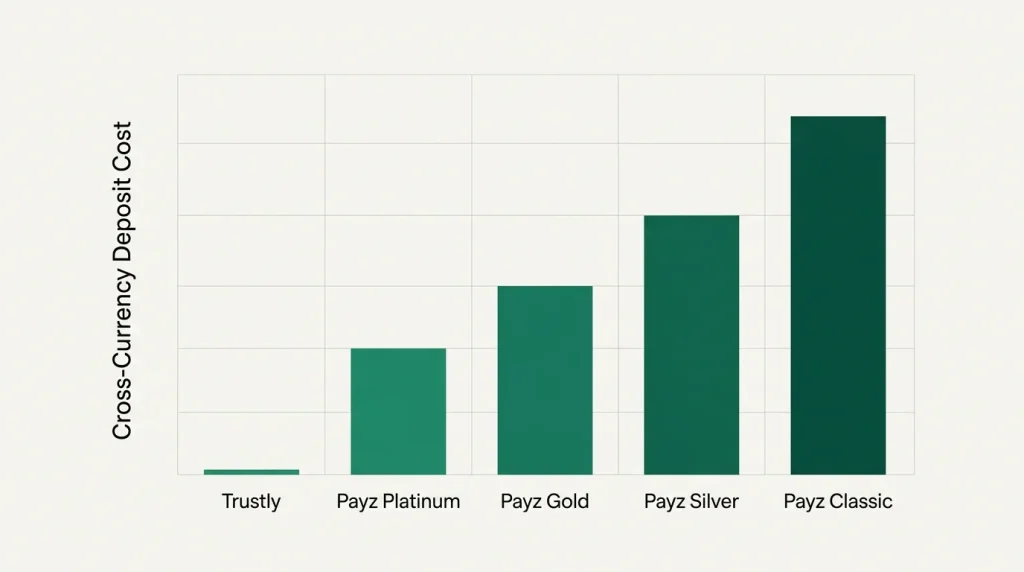

Payz charges the tier FX rate when currencies cross — 2.99% at Classic and Silver, 1.49% at Gold, 1.25% at Platinum and True VIP. No deposit fee on the wallet side. The Payz Mastercard has a £100 contactless ceiling per transaction in the UK, which can matter if you’re trying to pay a venue from the card rather than the underlying balance. Daily ATM cash limits run to €750 on the Mastercard, daily purchase limits to €5,500.

For a player depositing entirely in sterling at UK casinos that bill in sterling, Apple Pay is the cheaper rail because there is no FX. For any cross-currency exposure, Payz Gold and above tend to come out ahead on cumulative cost over a month.

Privacy and data sharing at the cashier

Apple Pay is often pitched as more private, and at one layer that’s true. The merchant never sees your real card number — only a token. Apple itself doesn’t store the transaction details on its own servers in a way that ties them to your identity. Good so far.

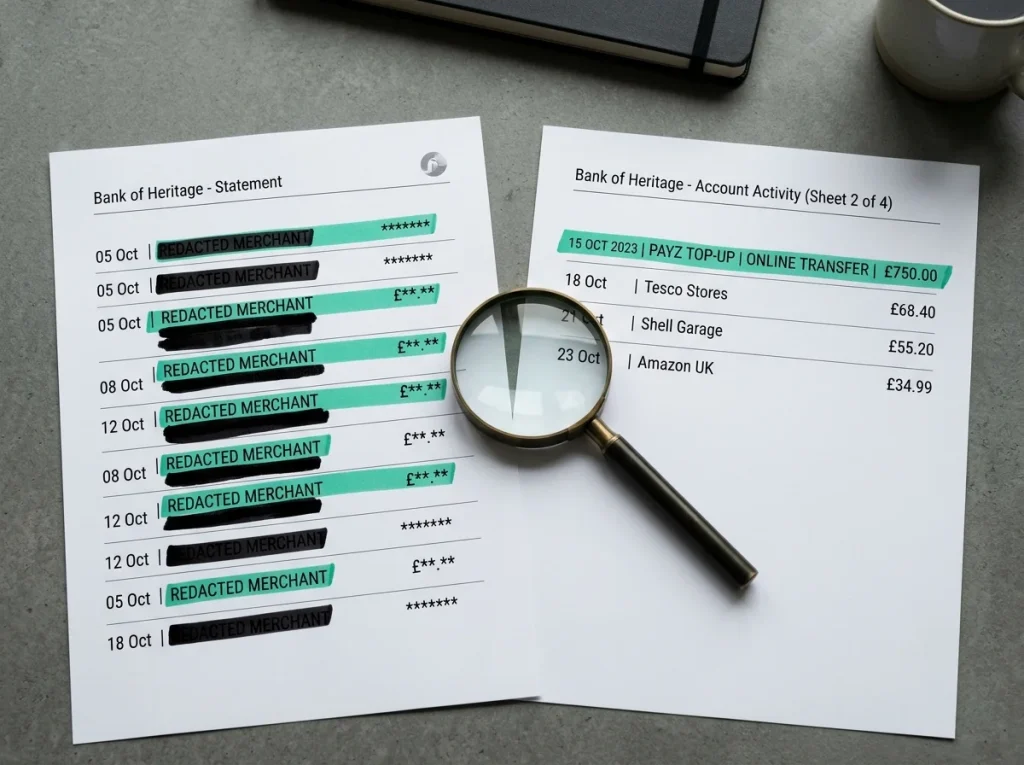

At the next layer, the privacy story is less clean. Your bank still sees every Apple Pay transaction tied to your account, with the merchant name, amount and category. Anyone who reviews your statement sees a casino name next to a Pay-by-Apple line.

Payz creates a layer of insulation. The casino sees Payz; your bank sees a top-up to PSI-Pay. The activity inside the Payz balance is private to Payz unless ordered by a regulator or court. For players who share bank statements with employers, landlords or mortgage advisors, this insulation can be the deciding factor. It isn’t anonymity — both wallets verify identity properly — but it is real privacy of activity from your routine bank statement.

Who each one actually suits

Apple Pay suits the player who deposits in sterling only, plays at well-established UKGC brands, doesn’t mind gambling appearing on a regular bank statement, and prefers the cleanest possible cashier flow on an iPhone. The friction is near-zero if your phone is already set up.

Payz suits the player who plays across multiple operators or currencies, wants the gambling activity insulated from routine bank statements, deposits often enough that maintaining a wallet balance pays for itself, or works with platforms where Apple Pay isn’t an option. The privacy benefit alone is worth the small setup overhead for many.

The hybrid setup is what I keep recommending: Payz as the primary rail for routine activity, with Apple Pay kept as a fallback for the occasional one-off deposit at a brand that supports it. That hybrid only makes sense once you’ve understood the underlying card debate, which I cover in my comparison of Payz against a direct debit card deposit — because Apple Pay is, beneath the tokenisation, ultimately a debit card transaction.

Does Apple Pay route through Mastercard like the Payz physical card, or differently?

Apple Pay routes through the underlying card you"ve loaded into the wallet — that might be Mastercard, Visa or American Express. The Payz physical card is its own Mastercard issued by PSI-Pay. The two only share a network if your Apple Pay default is a Mastercard, and even then the issuer and merchant relationships are different.

Which is more private at a UK casino — Apple Pay or Payz?

Payz adds a layer of insulation because the casino activity stays on the Payz balance, with your bank only seeing a single top-up. Apple Pay anonymises the card number to the merchant but leaves the gambling transaction visible on your bank statement at full detail. For day-to-day privacy from routine financial documents, Payz is the more private option.

ecoPayz Casino Articles: UK Market Trends and Payment Data

Created by the "Ecopayz Casino UK" editorial team.