ecoPayz vs Trustly: Compare UK Casino Transfer Speeds

Open Banking vs E-Wallet Rails: Structural Differences

I get this question every few weeks from clients who already use Payz and notice Trustly turning up in the same cashier panel. “It’s basically the same thing, right?” Wrong. They sit in the same column of the UI for the same reason supermarket shelves group different categories of milk together — convenience, not equivalence. The decision between them shapes the entire shape of a deposit, from the friction of the first click to the route a withdrawal takes home.

What's inside this guide

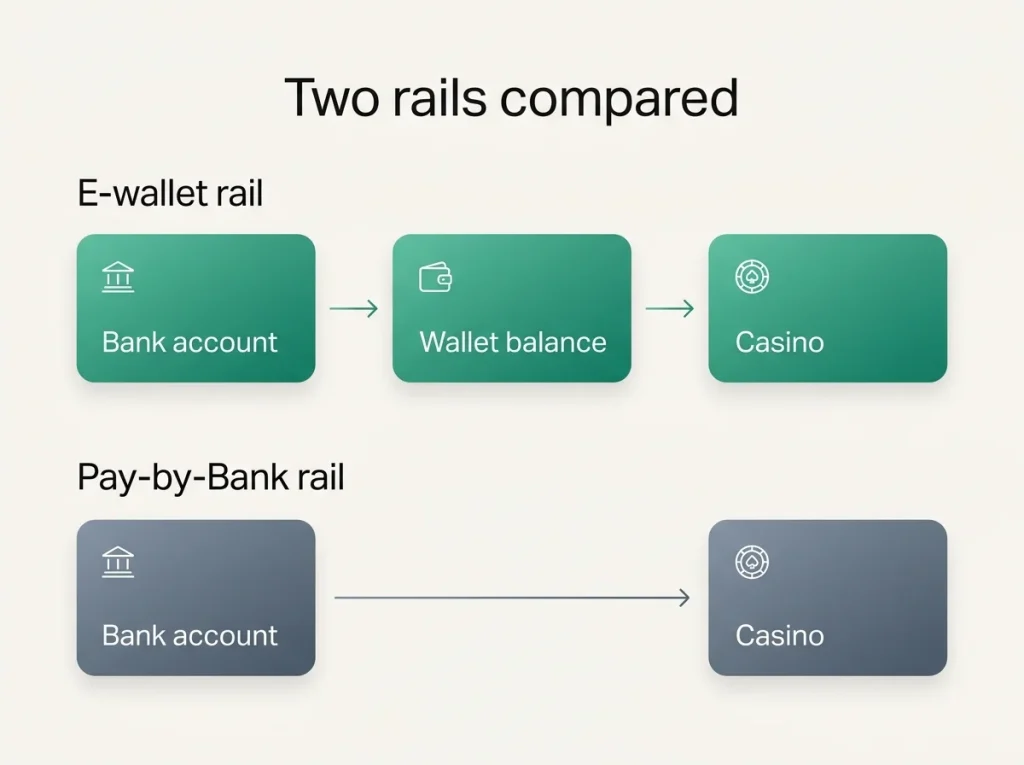

One is an e-wallet that holds a balance you fund and spend. The other is an Open Banking rail that moves money straight between your bank and the casino without ever holding it. The casino sees both as “instant deposit, low friction” — but the player feels the difference every time. With cash payments falling below 9 percent of all UK transactions for the first time in 2024, the wallet-versus-bank-rail decision is now the live one for British casino players. This walk-through is what I’d say to a friend over a pint instead of in a fee schedule.

The structural difference between an e-wallet and Pay-by-Bank

The cashier groups them. The plumbing doesn’t. Knowing the difference is the difference between picking a tool and being picked by it.

Payz is an e-wallet. You open an account, you fund it from a card or a bank transfer, the balance sits inside the PSI-Pay platform until you spend it. The casino sees Payz as an “external balance” — a pool of money it can debit when you authorise a deposit. After play, withdrawals route back into the Payz balance, where they sit again until you decide what to do with them.

Trustly is Pay-by-Bank. There is no stored balance. When you deposit, Trustly opens a one-time Open Banking session with your bank, authenticates you, and pushes money directly from your current account to the casino. Withdrawals reverse that — the casino instructs Trustly, Trustly arranges a bank credit back to the same account. Nothing sits in the middle. The 57% UK mobile-wallet adoption figure is often quoted as if e-wallets and Pay-by-Bank are the same category. They aren’t. Mobile wallets are part of that figure; Pay-by-Bank is closer to a wire transfer wearing a 2026 user interface.

That structural difference becomes the parent of every other comparison below — fees, friction, speed, KYC, all of it.

Fees and FX side by side

This is where the rails diverge sharply. The headline is simple enough: Trustly is usually free to the player; Payz has a transparent fee structure that bites only when currencies cross. The full picture is a little more interesting.

Trustly’s consumer-facing fee at UK casinos is almost always zero. The cost lives on the merchant side — the casino pays Trustly a percentage per transaction, and that’s absorbed into the operator’s margin. Where Trustly does cost you is opportunity cost: there’s no balance to earn anything on, and there’s no FX layer because both ends of the transaction are typically in GBP at a UK bank and a UK-licensed casino.

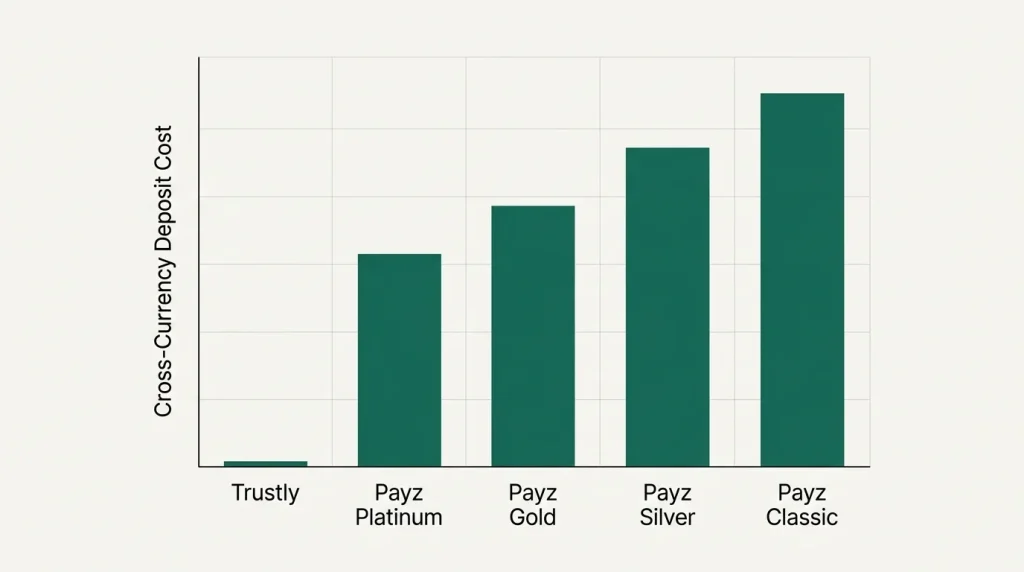

Payz charges a clear FX rate when currencies cross — 2.99% at Classic and Silver, 1.49% at Gold, 1.25% at Platinum and True VIP. No deposit fee on the wallet side, no withdrawal fee for transferring back to the Payz balance. The model is honest: if both sides of the transaction are GBP and your Payz balance is also in GBP, the cost is zero. If anything crosses currencies — a euro-denominated platform, a balance you happen to hold in another currency — the tier rate applies.

The arithmetic that matters: at low monthly volumes (under £200), the two are roughly equivalent in pure GBP play. Above that volume, Payz on Gold tier starts to compete with Trustly even on cross-currency play, because the 1.49% rate is small enough to disappear into noise. Where Payz pulls ahead is at any platform that bills in EUR or USD — Trustly can’t help you there in any meaningful way, while Payz holds multi-currency sub-accounts to mitigate the conversion entirely.

Deposit time and friction

“Instant” describes both. The path to instant is different.

A Trustly deposit starts at the casino cashier, redirects to a bank-selection screen, asks for online banking login (or biometric authentication through the bank’s app), and confirms. From first click to “deposit complete” usually runs 30 to 60 seconds if your bank app is already open on the same device. The friction is concentrated in the bank authentication step — and it can vary wildly between high-street banks and challenger banks.

A Payz deposit assumes you already have a funded Payz balance. From cashier to confirmation it’s typically 20 to 40 seconds, with no bank redirect involved. The friction is moved upstream — you had to fund the Payz wallet beforehand, which might itself have been a Trustly-style transfer at some point.

The practical conclusion: for a player who deposits a couple of times a month, Trustly is often the faster end-to-end path because there’s nothing to pre-fund. For a player who deposits weekly or more, Payz wins on the cumulative time saved — the wallet stays topped up, and individual deposits feel like spending balance rather than initiating a transfer.

Withdrawal time and friction

Both will tell you “instant withdrawal” on the marketing page. Both lie a little. The casino-side review consumes the same six to forty-eight hours no matter which rail you use.

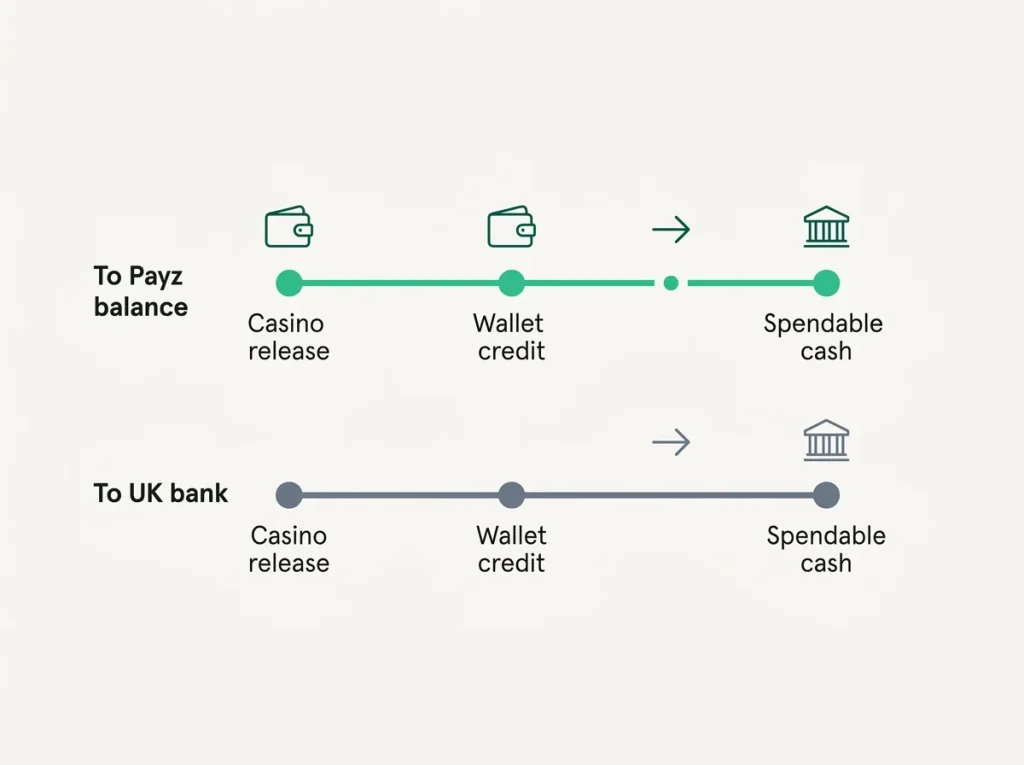

After casino release, the divergence is real. Trustly typically credits a UK bank account within a few hours, sometimes the same minute on Faster Payments-enabled banks. The money lands in a place you can spend from directly — a current account or savings account — without another step.

Payz credits the Payz balance within an hour, often within minutes. But that’s a holding pen, not a spending account. To get the cash to a real bank account, you’ll either need to push it onward through the Payz Mastercard (T+1 business day) or trigger a withdrawal to a linked bank (another one to three days). For some players that holding pen is a feature — it prevents a quick re-deposit. For others it’s an extra hop.

Net: Trustly is usually faster end-to-end on a single cashout. Payz is more useful if the money is going to fund the next deposit anyway, because it sits ready.

KYC on each rail

KYC is where the rails feel most different in practice. Both wallets sit downstream of the casino’s own KYC stack, so the operator will always run its own checks on you. The wallet-side checks layer on top.

Trustly performs almost no consumer-facing KYC. The model relies on your bank having already done it — your bank knows who you are, where you live, what your income is. Trustly trusts that and adds nothing visible to the player.

Payz runs a tiered KYC of its own. Classic is light-touch — name, address, email. Silver adds proof of identity. Gold and above add proof of address, source of funds and sometimes source of wealth. Higher tiers unlock larger limits and lower fees. That’s a structural cost: more documents in, more capacity out.

For a player who already has Gold or higher Payz status from a previous cycle, the dual-KYC stack is invisible. For a brand-new account, Trustly is a softer first contact — log in to your bank, deposit, done.

Picking the right rail for your habits

Use Trustly when you deposit irregularly, value zero pre-funding, want money back in your bank account rather than a wallet, and only ever play at GBP casinos. The friction of bank authentication per session is offset by the simplicity of not maintaining a separate balance.

Use Payz when you deposit weekly or more, you play across multiple casinos or currencies, you want a per-deposit FX rate that’s predictable, or you need a buffer balance between your bank account and your gambling activity. The wallet’s holding-pen effect on withdrawals genuinely changes spending patterns, which some players want and others don’t.

Many of my clients run both — Trustly for the rare large deposit, Payz for the routine weekly play. Adding a third rail on top, like a contactless mobile wallet, opens further questions, which is why my comparison of Payz against Apple Pay is worth pairing with this one before locking in your default.

Does Trustly"s bank-to-bank model expose my Payz balance to the casino in any way?

No. Trustly and Payz are independent rails. Using Trustly for a deposit transfers funds directly from your linked bank account to the casino without touching the Payz wallet. The casino sees a Trustly transaction; your Payz balance is untouched and invisible in that flow.

Which is faster at the average UK casino — Trustly withdrawal or Payz withdrawal?

End-to-end Trustly is usually faster to a usable bank account because there is no intermediate wallet step. Payz is faster to its own balance, often within minutes, but reaching a current account from there adds a card-payout or bank-transfer step. The casino-side review takes the same time either way.

ecoPayz Casino Articles: UK Market Trends and Payment Data

Published by the Ecopayz Casino UK team.