ecoPayz vs Debit Card: UK Casino Deposit Comparison

Market Shift: Banking Options After the Credit-Card Ban

I had a client in Manchester who simply refused to believe me when I told him, in April 2020, that his credit card would never work at a UK casino again. He pulled out his Barclaycard, tried it three times in a row at his usual operator, and got declined each time. That was the day the UK gambling industry’s payment landscape locked into its current shape. Credit cards were out — fully, with no carve-outs. Debit cards stayed. E-wallets like Payz quietly took over a chunk of the volume that had once flowed through plastic with a credit line behind it.

What's inside this guide

The choice, six years on, is between funding casino activity directly from a UK debit card or routing it through Payz first. Both are legitimate. Both are widely accepted. The trade-offs are real and underestimated — and they shape everything from fee exposure to what happens when something goes wrong. Mobile-wallet adoption now covers 57% of UK adults, but a clear majority of casino deposits still start at a debit card somewhere in the chain. Understanding when each path makes more sense is the question this piece exists to answer.

How the credit-card ban reshaped the deposit landscape

On 14 April 2020, the UK Gambling Commission banned credit card deposits on all licensed gambling sites, with no transitional period and no exceptions for small operators. The reasoning was straightforward: too many players were running up gambling debts on borrowed money, and the harm metrics were too consistent to ignore. Since that day, debit cards, e-wallets and bank transfers have covered the full 100% of UK gambling deposit volume.

The migration didn’t happen evenly. Debit cards absorbed the largest share — they were already the most common payment method, and the operational change for the player was minimal. E-wallets took the next biggest slice. Payz, Skrill and Neteller all saw their UK gambling volumes climb through 2020 and 2021. Bank transfers and Pay-by-Bank rails like Trustly took the third slice, smaller but growing.

What’s worth noticing is what the ban didn’t do. It didn’t stop the borrowing — it stopped one specific channel for it. A determined player can still fund a debit-card deposit from an overdraft, from a personal loan that lands in their current account first, or from a buy-now-pay-later product if the merchant accepts it. The regulator’s logic was that adding friction to one of the most direct paths would reduce harm at the margin, and that has played out roughly as expected. For payment-method choice, the practical consequence is that debit cards are now the default, and any alternative — Payz included — is competing against debit cards rather than against credit cards.

How each processing path actually works

The two paths look identical at the cashier. Behind the cashier they aren’t.

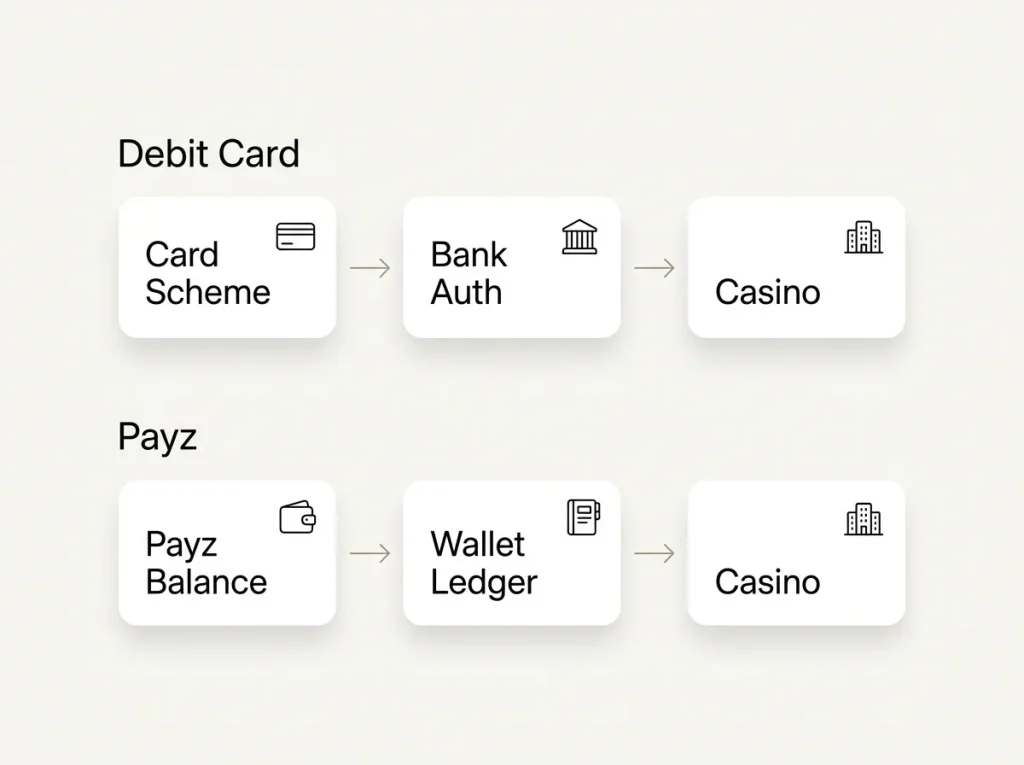

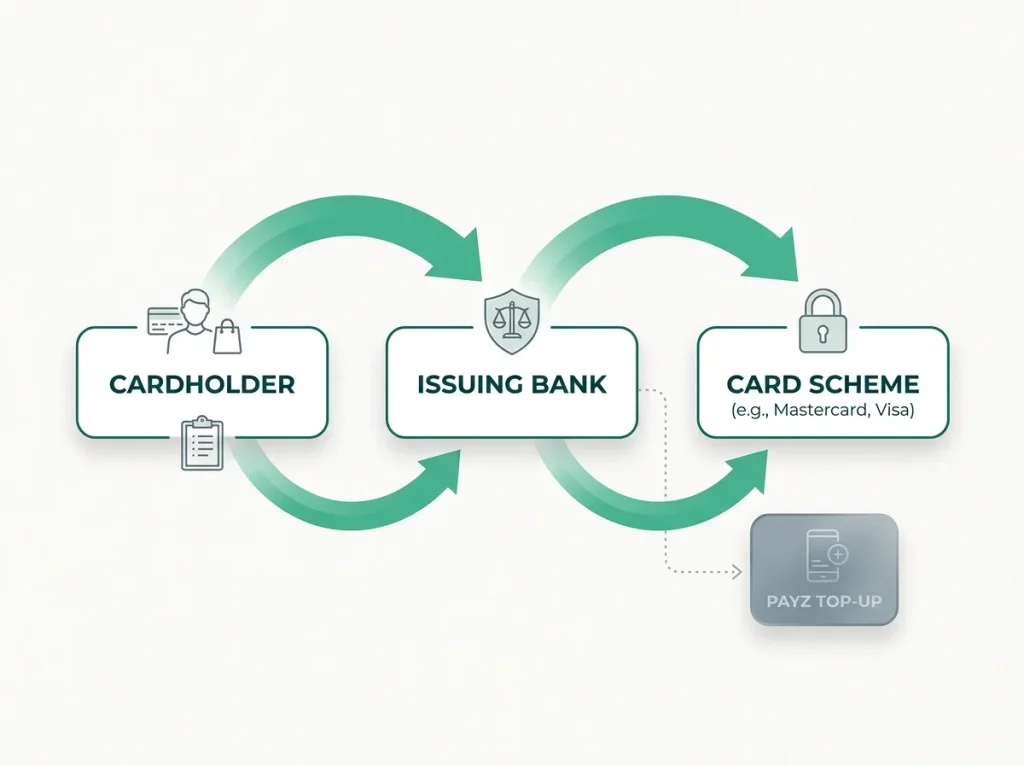

A debit card deposit goes from your card scheme (Visa or Mastercard) through your bank’s authorisation system to the casino’s acquirer, then back to the casino’s account. The whole loop completes in seconds. Your bank sees the merchant name, the gambling category code, and the amount. Roughly 18.9 of the 26.1 billion UK debit card payments in 2024 were contactless, but only a small fraction of those were gambling-related — gambling deposits skew toward card-not-present entries online.

A Payz deposit assumes a funded Payz balance. The cashier debits the Payz balance directly through the PSI-Pay platform. Your bank only sees the original top-up to Payz, not the eventual casino deposit. The two-step structure — fund the wallet, then spend from the wallet — creates a buffer that affects both privacy and fee exposure, in different ways for different players.

For first-time deposits, the debit-card path is almost always faster end-to-end. For routine play, the Payz path is faster per session because the balance is already in place.

Fees and FX side by side

This is the heart of the comparison.

Debit cards at UK casinos generally carry no consumer-facing fee — the operator pays interchange to the card scheme and absorbs it. Foreign-currency conversion does add a fee, typically 2% to 3% over mid-market, charged by your card issuer. UK casinos billing in pounds avoid that fee entirely; international platforms billing in EUR or USD trigger it. Daily card limits are set by your bank and vary widely.

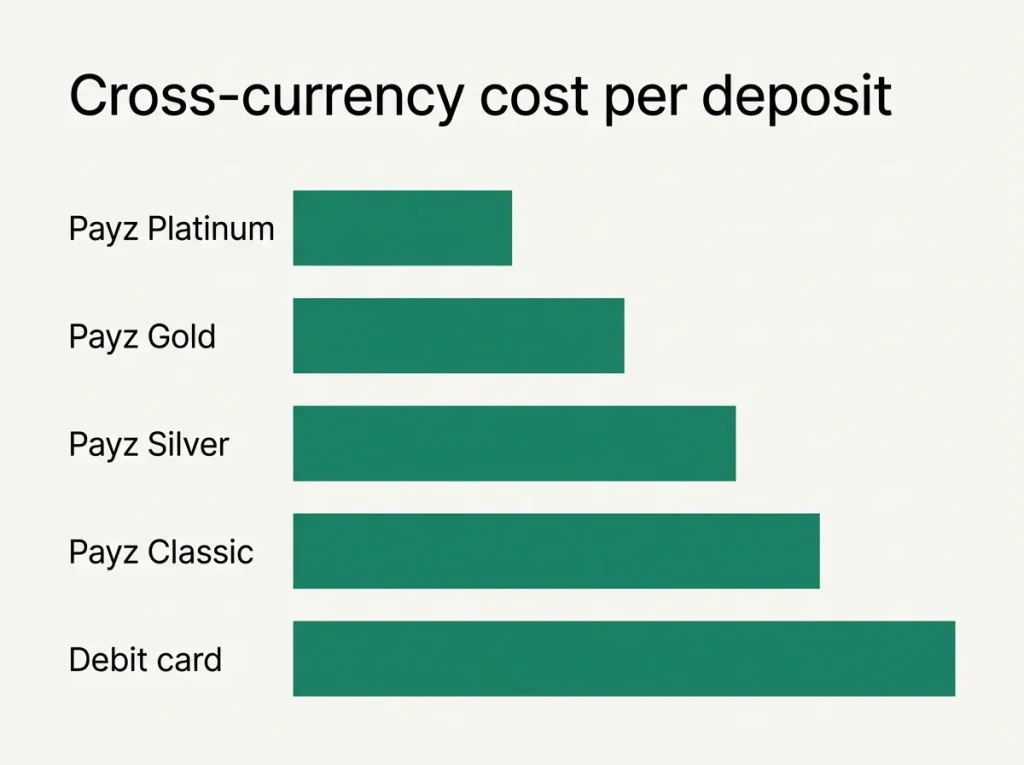

Payz charges no deposit fee at the wallet side. The FX layer is the tier rate: 2.99% at Classic and Silver, 1.49% at Gold, 1.25% at Platinum and True VIP. If your Payz balance is GBP and the casino bills GBP, the FX is zero. If anything crosses, the tier rate applies — and importantly, the rate is published and predictable, unlike most card-issuer FX margins which are buried in monthly statements.

The arithmetic that matters: at small volumes (single deposits under £50) and pure sterling settlement, a debit card is marginally cheaper because there’s nothing to charge against. At larger monthly volumes with any cross-currency exposure, Payz at Gold or above wins because the published rate beats most card-issuer FX margins. Mid-volume sterling-only play sits in a band where the two are roughly equivalent.

Bonus eligibility and stake-cap interaction

UK casinos generally exclude e-wallet deposits from welcome bonuses. They generally do not exclude debit card deposits. That’s the simplest summary, and it matters most to new accounts.

If your goal is to qualify for a sign-up offer, a debit card deposit is the cleaner path at most operators. The exclusion clause that catches Payz — and Skrill, Neteller, PayPal, all the e-wallets — typically doesn’t apply to a Visa or Mastercard debit transaction. There are exceptions in both directions: a small set of operators excludes both, and another small set excludes neither. Read the specific terms before depositing.

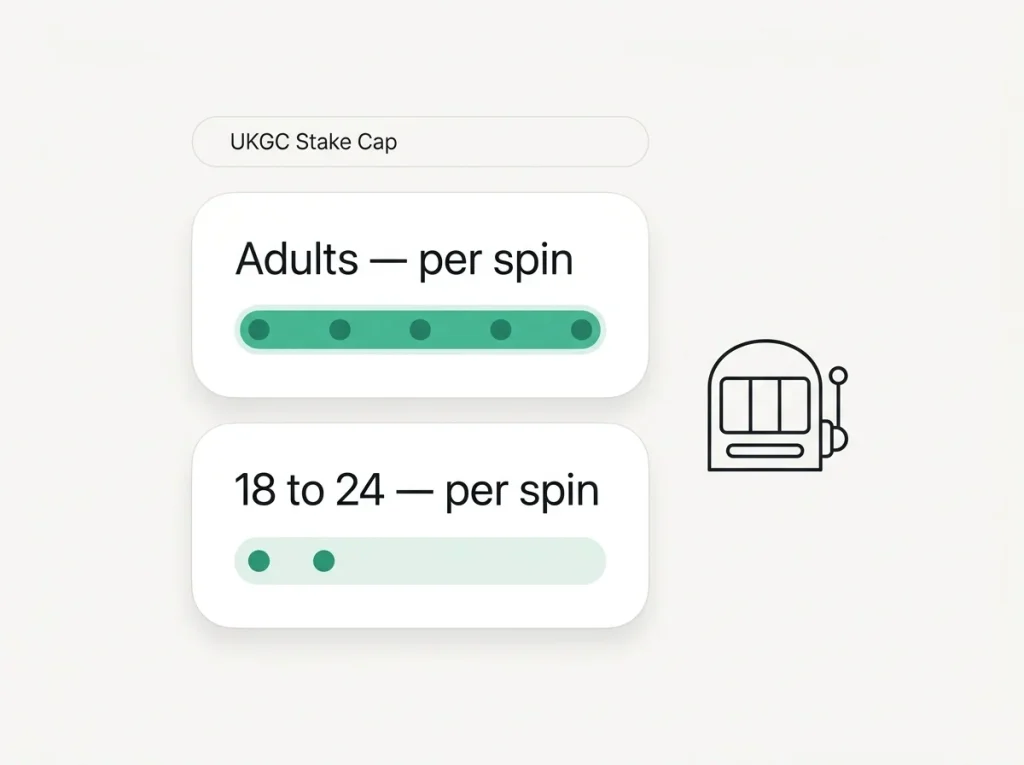

The stake-cap rules introduced in 2025 — £5 per game cycle for adults, £2 for 18 to 24 year olds — apply equally to both deposit methods. They’re enforced at the slot level, not the cashier level. A £100 Payz deposit and a £100 debit card deposit both face the same per-spin ceiling on online slots. The cap reshapes session length more than deposit size, and that effect is independent of whether the money entered the casino via a wallet or a card.

Chargeback rights — the asymmetry worth knowing

Here’s where the two paths separate most sharply, and it’s the part most players never check until they need it.

A debit card transaction can in principle be disputed through your bank under card-scheme chargeback rules. In gambling, the success rate is low — the merchant can show you authorised the transaction, played the game, and received the service — but the right to dispute exists. UK debit card chargeback rights extend to fraudulent transactions and a narrow band of service failures.

A Payz top-up funded by debit card preserves a chargeback path against your bank if the top-up itself is disputed. The casino deposit from the Payz balance, however, doesn’t have a card-scheme chargeback at all — it’s a direct e-money transaction, not a card payment. If something goes wrong at the casino end, your route is through the casino’s complaints process and ultimately through IBAS or the Gambling Commission, not through Visa or Mastercard.

That asymmetry is the strongest single argument for direct debit-card deposits at higher-risk operators. For UKGC-licensed casinos with established track records, the practical difference is small, but it isn’t zero. The broader safety picture — including FCA safeguarding rules covering the Payz balance itself — is covered in my fuller review of whether Payz casinos are safe under UKGC and FCA rules.

Choosing the rail for your specific habits

Pick the debit card directly if your priorities are bonus eligibility, chargeback rights, single-deposit simplicity, and sterling-only play at a UK casino you already trust. The setup is zero — your card already works.

Pick Payz if your priorities are gambling activity insulation from your routine bank statement, predictable FX on cross-currency casinos, the ability to set a wallet-side spend cap separate from your bank balance, or the convenience of a topped-up balance for frequent small deposits. The setup cost is real but one-time.

The asymmetric answer most experienced players land on: debit card for the first deposit at any new operator (to preserve chargeback and bonus rights), Payz for routine play once the operator has earned trust. That two-stage default is what I write into most client setups.

Can a UK debit card chargeback recover money lost to gambling if Payz was the intermediary?

No. A chargeback only applies to the card-scheme leg of the chain. If your debit card funded a Payz top-up, you can dispute that top-up with your bank in limited circumstances — but the subsequent Payz-to-casino transaction is an e-money payment and has no card-scheme chargeback at all. Disputes about the casino itself go through the operator"s complaints process and IBAS, not the card scheme.

Does the £5/£2 stake-cap interact differently with debit-card vs Payz deposits?

No. The stake cap is enforced at the game level, not the deposit level. A £100 deposit by either method faces the same £5 per spin limit for adults or £2 for 18 to 24 year olds on online slots. The deposit method has no effect on the cap itself.

ecoPayz Casino Articles: UK Market Trends and Payment Data

Written by the editors at Ecopayz Casino UK.