ecoPayz Classic Tier: UK Casino Limits and FX Rates

Classic Tier Profile: Baseline Limits for Casual Players

I’ve watched plenty of casino players panic-upgrade their Payz account to Silver or Gold within their first month, only to never actually use the extra headroom. The Classic tier carries an unfair reputation in player forums — too restrictive, too clunky, too “starter pack” — and most of that reputation is based on the limits at sign-up rather than the limits after verification. Once you understand how the tier really behaves, the decision to stay on it or move up gets honest.

What's inside this guide

This piece walks through what Classic actually unlocks at UK casinos, where the limits start to bite, and the specific monthly spend pattern at which moving up genuinely saves money. If you’re still figuring out whether you’ll be a £40-a-month casino player or a £400-a-month one, Classic is almost certainly the right starting point — and the path to Silver, when needed, is short.

What the Classic tier actually is inside the Payz structure

Classic is the default tier you land on the moment a Payz account opens. It’s not a stripped-down version of the higher tiers — it’s the same wallet, with the same regulatory protection from PSI-Pay’s FCA authorisation, just with different limits and a different fee profile. The wallet ledger, the Mastercard option, the casino integrations, the security features — all are identical to what a Gold-tier user sees.

What differs is the ceiling and the cost-per-transaction. Classic limits are tighter than Silver, Silver is tighter than Gold, and so on up to True VIP. The FX rate at Classic matches the rate at Silver (2.99%), then drops at Gold (1.49%) and again at Platinum and True VIP (1.25%). The casino-side experience is identical regardless of tier — when you fund a deposit, the cashier doesn’t display which tier you’re on. The differences only become visible at the wallet end, in your monthly limits and your conversion costs.

Most British casino players I see start on Classic, run there for one to three months, and only move up when a specific limit or fee starts genuinely hurting. That sequence — start light, upgrade only on need — is what I’d recommend by default.

The actual limits at Classic for casino play

The numbers most casino players need to know are the annual and per-transaction caps. Classic carries a relatively low annual top-up ceiling — sufficient for a few thousand pounds of activity per year but not for high-frequency play. Daily and monthly caps on inbound funding are also more restrictive than the higher tiers.

On the spending side, you can still send Payz to UK casinos without hitting the wallet-side cap on most days. The pinch points are usually inbound: you’d hit a monthly funding ceiling before you’d hit a monthly spending ceiling. That sequence matters because it tells you which limit is going to bite first.

The Payz Mastercard, available at Classic if you order one, carries a £100 contactless ceiling per transaction in the UK — same as the higher tiers, because that’s a Mastercard scheme rule rather than a Payz-imposed one. For ATM cash withdrawals, the Classic-tier daily limit is lower than at Gold and above. For online card-not-present purchases (which includes some casino cashier flows that take the physical Mastercard number rather than the wallet ID), the daily and monthly caps again sit at the lower end of the tier range.

If you’re depositing £20 to £50 at a single casino once or twice a week, Classic limits will never trouble you. If you’re moving £200 a week across multiple operators, expect to bump into a monthly inbound funding ceiling within six to eight weeks.

The FX rate impact on real casino deposits

The headline number is 2.99% — the Classic-tier FX rate, applied whenever your Payz balance currency differs from the casino’s billing currency. The same rate applies at Silver. Gold cuts it to 1.49%; Platinum and True VIP to 1.25%.

For a UK-resident player with a GBP-funded Payz balance playing at a GBP-billing UKGC casino, the FX rate is irrelevant — there is no conversion, so there is no fee. The 2.99% only kicks in when the casino bills in a different currency, which happens at platforms with corporate addresses outside the UK or at multi-currency operators that default to EUR.

What 2.99% costs in real money: a £100 deposit at a EUR-denominated casino costs about £3 in conversion. A £400 monthly volume costs about £12. Over a year, a player averaging £300 per month at cross-currency casinos pays about £108 in FX at Classic. That same player at Gold would pay about £54. The £54 saving has to be weighed against Gold’s monthly subscription fee — which is the calculation the next paragraph and the upgrade-trigger section walk through.

At pure sterling play, the 2.99% Classic rate is invisible. At hybrid play with occasional foreign-currency exposure, it adds up slowly. At consistent cross-currency play, it adds up faster than most players notice, and that’s the line where upgrading starts to make arithmetic sense.

The KYC actually required at Classic

Classic onboarding requires the lightest KYC of any Payz tier. Name, date of birth, address, email and a phone number are usually enough to open the account. No ID upload, no proof of address, no source-of-funds questionnaire. The whole sign-up takes under ten minutes if you have your details to hand.

There’s a caveat. Classic-tier limits are tight enough that PSI-Pay can run on the regulatory minimum check. The moment you try to push past those limits — by depositing larger sums or by aggregating volume above a threshold — you’ll be prompted for the Silver upgrade documents. That isn’t a punishment; it’s the FCA-mandated step that opens higher limits.

At the casino end, the operator’s own KYC is independent of your Payz tier. A new casino account will ask for ID, proof of address and sometimes source of funds before any withdrawal regardless of which Payz tier funded the deposit. The two stacks run in parallel — being verified at Payz doesn’t satisfy the casino, and vice versa.

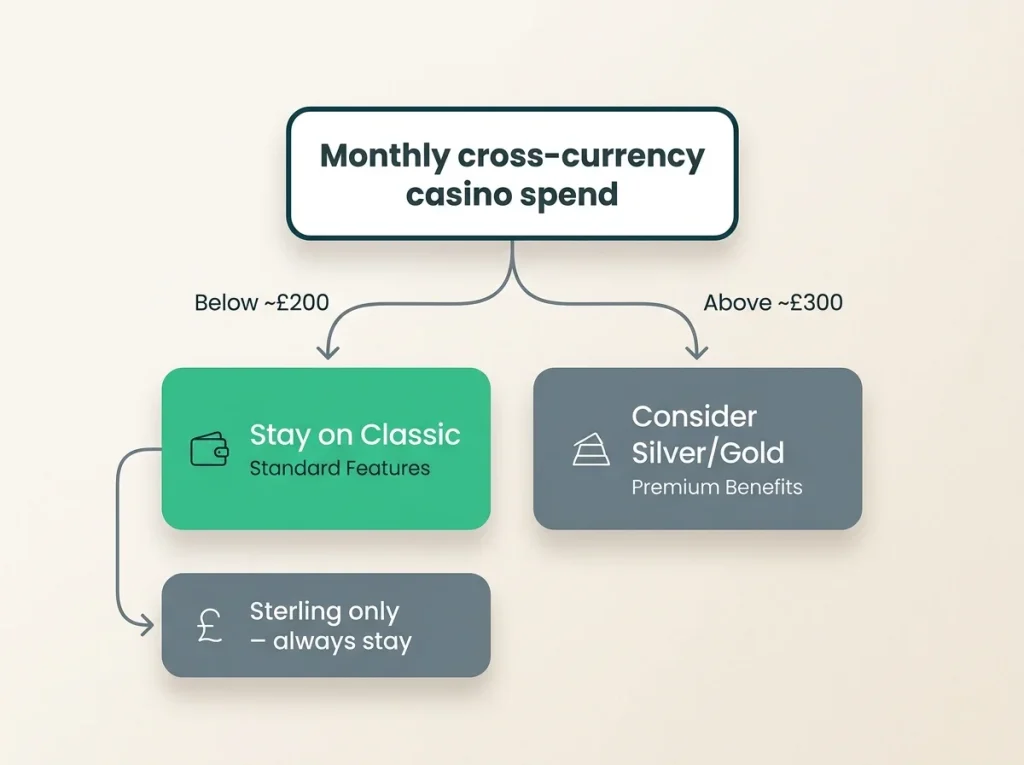

When Classic is genuinely the right tier for casino play

I’d tell a player to stay on Classic if their monthly casino spend sits under £200, their play is concentrated at GBP-billing UKGC casinos, they don’t yet know whether they’ll keep playing in six months, or they want the wallet light and free to close without unwinding higher-tier subscriptions. The combination of zero monthly fee at Classic and the same FCA protection as the higher tiers makes it a sensible default.

The triggers to move up: monthly cross-currency volume above £300, repeated bumping against Classic’s inbound funding ceiling, or a desire to use the Payz Mastercard for larger ATM withdrawals than Classic allows. Once one of those triggers appears consistently for two months, the Silver upgrade is usually worth it — and from Silver, the path to whether Silver itself justifies the next jump to Gold opens up.

Can I deposit at a UK casino on a brand-new Classic Payz account before any ID upload?

Yes, within the Classic-tier limits. The account is functional from the moment registration completes — name, address, email and phone are enough for entry-level Classic limits. You"ll only be prompted for ID upload if you try to push past those caps or trigger any AML flag. Casino-side KYC is separate and still applies.

At what monthly casino spend does staying on Classic actually cost more than upgrading?

For pure GBP play at UK casinos, Classic stays free indefinitely because the FX rate never triggers. For cross-currency play, the breakpoint is roughly £300 per month — above that, the Gold tier"s lower FX rate starts saving more than the Gold monthly fee costs. Silver doesn"t change the FX rate from Classic, so the only reason to move to Silver is for limit headroom, not fees.

ecoPayz Casino Articles: UK Market Trends and Payment Data

Prepared by the Ecopayz Casino UK editorial staff.