ecoPayz Casino KYC Verification: Mandatory Document Checks

Dual KYC Friction: Clearing Casino and E-Wallet Checks

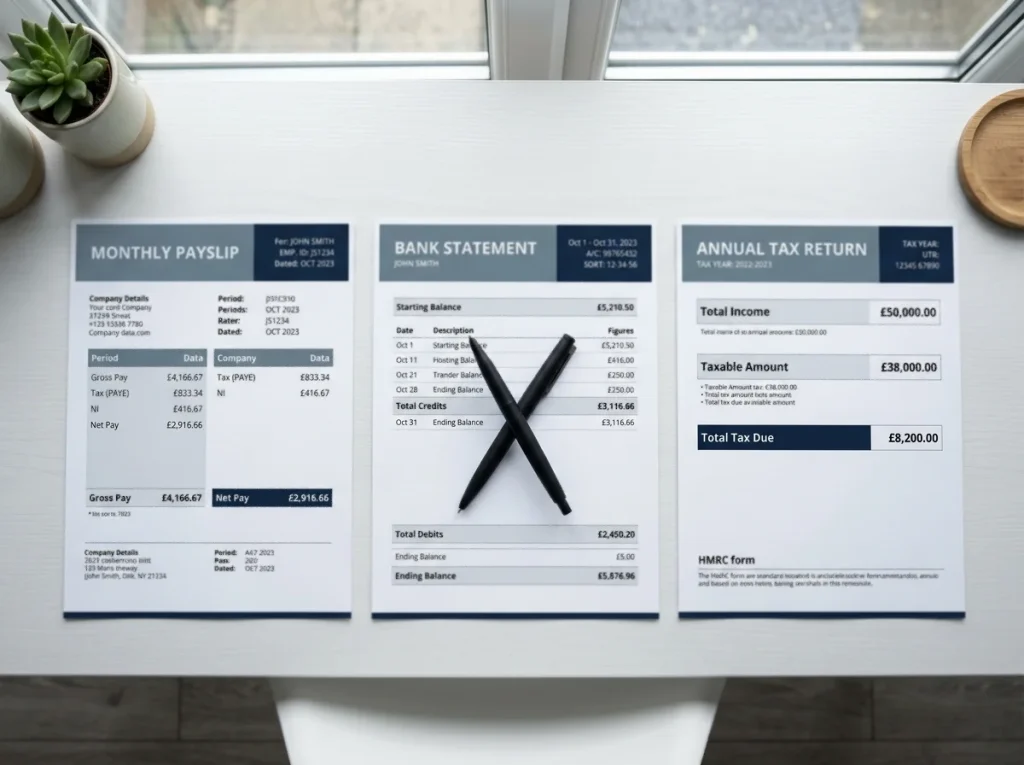

A player I corresponded with last autumn had verified his Payz account to Gold tier, completing every Payz-side document check including passport, proof of address and a source-of-funds declaration. He then registered at a UKGC-licensed casino, deposited £50 via Payz, won £400, requested a withdrawal, and was promptly asked for his passport, his proof of address, his bank statement and a salary slip. “But Payz already has all of this,” he wrote. “Why does the casino want it again?”

What's inside this guide

The short answer is that Payz’s KYC and the casino’s KYC are entirely separate stacks operating under different regulatory regimes. The casino doesn’t see what Payz has verified. Payz doesn’t see what the casino has verified. Both verifications are mandatory, and the most efficient way to play with Payz at UK casinos is to understand each one on its own terms. The cost of getting this wrong has become very visible – UKGC enforcement actions in 2025 included a £2,022,000 fine against Spreadex and a £650,000 fine against NetBet, both touching on AML and KYC control failings.

Two separate KYC stacks, both mandatory

The Payz KYC stack is run by PSI-Pay under its FCA authorisation as an Electronic Money Institution. The casino KYC stack is run by the operator under its UKGC operating licence. These are two different regulators, two different rule books, and two different obligations.

From the Payz side, the verification builds towards account tier. A new Classic account requires basic identity proof to operate at the lowest limits. Moving up – Silver, Gold, Platinum, VIP – requires progressively more documentation: proof of address, source of funds declarations, sometimes a face-to-face or video verification step at the highest tiers. The wallet uses this to manage its own AML obligations and to set the appropriate transaction limits for each account.

From the casino side, the verification is driven by the UKGC’s licensing conditions and codes of practice. The operator has to confirm identity, age, address and self-exclusion status before allowing wagering. They have to monitor for problem gambling indicators and apply AML checks proportionate to the player’s activity. None of these obligations are satisfied by Payz’s prior verification, because the casino is a separate licensee with its own accountability.

The practical effect for players is double documentation. You’ll submit passport scans to both. You’ll submit proof-of-address utility bills to both. If your activity warrants it, you’ll submit bank statements or salary slips to both. The two systems don’t share data, and there’s no mechanism to “import” your Payz verification into a casino’s records.

Payz-side documents at each tier

The Payz tier ladder dictates what the wallet asks for, and the documents stack rather than reset as you climb. At Classic – the entry tier – you provide name, date of birth, address and a basic identity check, usually a passport or driving licence scan plus a recent utility bill or bank statement. This is enough to operate within Classic limits but caps your activity at relatively modest transaction sizes.

At Silver, the wallet wants the same identity documents to a higher confidence standard plus a confirmed funding source. If you’ve linked a debit card or bank account, that linkage counts towards the Silver verification. The wallet also runs an enhanced check against UK identity registers at this stage.

At Gold, the FX rate drops from 2.99% to 1.49% but the documentation requirement increases. Payz typically asks for a source-of-funds statement – where your money comes from, in narrative form – plus supporting evidence such as a recent payslip, tax return or bank statement showing regular income. For self-employed players, the documentation tends to be more involved. The wallet may also conduct a video verification call at this tier, where a representative confirms you holding your ID document.

At Platinum and VIP, the rate falls again to 1.25% and the verification becomes more bespoke. PSI-Pay typically assigns a dedicated account manager at these tiers and the document chain becomes more of a continuous conversation than a single onboarding event. PSI-Pay is a Mastercard Principal Member since 2009 with total assets of £64.97m, which means the firm holds the regulatory permissions and resources to operate full-scale enhanced due diligence at the top end of the tier ladder. The further you go, the less the verification looks like a form-filling exercise and the more it resembles a private-banking style onboarding.

Casino-side KYC triggers

UK casinos don’t run full KYC on every player at registration. They run a basic identity verification at sign-up – name, date of birth, address, age – and they re-trigger deeper checks based on a list of events that vary slightly between operators but follow a predictable pattern.

The first-deposit threshold triggers verification at most operators. A casino allowing £10 minimum deposits may run automated checks instantly on first deposit and only ask for documents if the automated check fails. Higher deposits cross thresholds for enhanced due diligence under the operator’s AML programme. £2,000 cumulative is a common trigger; £5,000 is almost universal.

The withdrawal trigger is the one most players encounter. First withdrawal on an account routes through manual review at most UK operators, and that review almost always asks for ID documents and proof of address even if those have already been provided at registration. The pattern repeats on any unusual withdrawal – large amount, new device, change in deposit method, unusual session timing.

Activity pattern triggers are the least visible. Operators monitor for patterns consistent with bonus abuse, account sharing, money laundering, or problem gambling, and any of these can trigger an out-of-band document request. The UKGC Director of Enforcement John Pierce framed this directly when announcing the Videoslots action: “Operators are required to have effective Social Responsibility and Anti-Money Laundering policies, procedures and controls as a condition of holding an operating licence … the operator’s monthly deposit limits were found to be ineffective when tested in practice and AML controls were not applied to the standards we expect.” The Spreadex £2,022,000 fine that same year was largely about exactly this gap. Operators that don’t ask for documents proactively are increasingly the ones the regulator pursues, which is why the trend in UK casino KYC is towards more requests rather than fewer.

Source-of-funds checks

Source-of-funds is the part of casino KYC that catches even experienced players off-guard. A standard identity check confirms who you are. A source-of-funds check asks where your money came from, and the answer has to be documented.

The trigger for a casino-side source-of-funds review is usually cumulative deposit volume rather than any single transaction. The NetBet £650,000 fine in 2025 cited gaps in this area specifically – players who had crossed deposit thresholds without proper source-of-funds documentation being collected. Since then most operators have tightened their automated triggers.

The documents requested vary by player profile. Salaried employees typically provide a recent payslip plus a bank statement showing the salary deposit. Self-employed players need accountant-prepared income statements, tax returns or business bank statements. Players with non-employment income – investments, inheritance, property sales – need documentation specific to that source. The chain of evidence has to make sense: a £15,000 monthly deposit volume needs an income source that plausibly supports it, and the documents have to demonstrate that link.

Payz’s own Gold-tier source-of-funds review covers similar territory but is a one-time event rather than an ongoing audit. The casino’s version is continuous – the operator reserves the right to ask again at any future trigger event, and refusing or providing inadequate documentation can freeze withdrawals indefinitely.

Common rejection reasons and how to avoid them

The single most common rejection reason on both sides is a mismatch between submitted documents. The name on the passport doesn’t match the name on the utility bill because one shows a middle name and the other doesn’t. The address on the bank statement is three months old and shows a previous address. The proof of identity is a photo of a screen rather than a clean scan or photograph of the physical document. None of these are sinister; all of them require resubmission.

The second pattern is recency. UK KYC requires proof of address dated within three months for most operators, sometimes two months for higher-tier checks. A utility bill from six months ago will be rejected even if everything else is correct. The fix is to use whichever utility you receive most frequently and to download the latest bill the moment a casino asks.

The third pattern, specific to Payz-and-casino combinations, is registered-address mismatch. If the address on your Payz account differs from the address on your casino account, both verifications can fail. UK operators sometimes cross-check the address on the funding wallet against the address on the casino registration, and a mismatch flags as a potential account-sharing or fraud indicator. Keeping the Payz address and the casino address identical, with matching utility-bill documentation, eliminates this entire class of friction. The sign-up itself, where the address is first set, is covered in the walkthrough of registering a Payz account and making the first casino deposit.

Can I use one set of KYC documents for both Payz and the casino, or must each verify separately?

Each verifies separately. The two systems don"t share data, and there"s no mechanism to pass verification status from one to the other. You"ll submit identical or near-identical documents to both, but each one runs its own check under its own regulatory regime.

Why does a casino re-request ID even after Payz has already verified me to Gold tier?

The casino has no visibility into what Payz has verified and operates under a separate UKGC licence with its own KYC and AML obligations. Even Gold-tier Payz verification does not satisfy the casino"s licensing conditions, so the casino runs its own complete check.

What happens if my Payz address and my casino account address don"t match?

Both verifications can fail. The mismatch is treated as a potential fraud or account-sharing indicator. Update one to match the other before submitting documents to either side, and ensure your proof-of-address evidence supports whichever address you use across both.

ecoPayz Casino Articles: UK Market Trends and Payment Data

Created by the "Ecopayz Casino UK" editorial team.